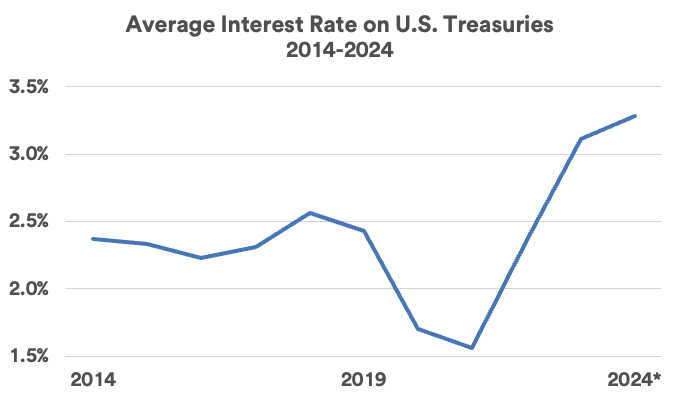

“Initially, higher bond yields reflected rising inflation,” says Bill Merz, head of capital market research at U.S. Bank Wealth Management. However, even with inflation reduced from peak levels, rates stayed elevated due to a stronger than expected economy and delays in potential Fed rate cuts, according to Merz. He says another key factor that can affect bond yields, “is the supply of bonds relative to the demand by bond buyers.” If the Treasury needs to issue more bonds, that results in greater supply. “In that event,” says Merz, “more supply might result in buyers demanding higher interest rates to absorb the expanded issuance.”

The U.S. Treasury borrowed $748 billion in the first quarter of 2024 and another $234 billion in the second quarter. It projects a need to borrow an additional $740 billion in the third quarter, which is more than $100 billion less than it initially projected. The Treasury currently estimates that fourth quarter 2024 borrowing will add another $565 billion in privately-held net marketable debt. 3

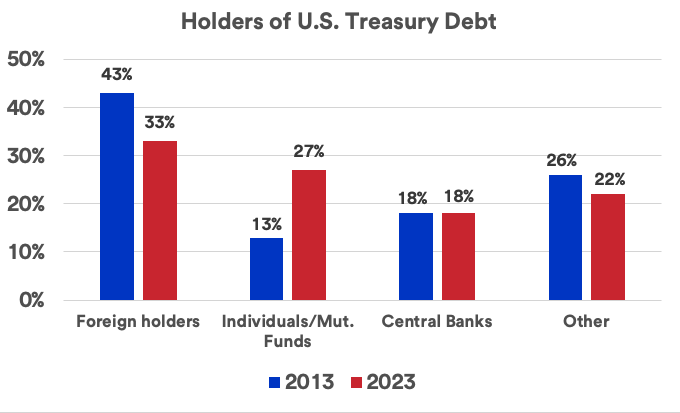

While Treasury debt supply expands, concerns were raised over a potentially shrinking pool of Treasury buyers. Most notable is the Fed, which began a “quantitative tightening” strategy, winding down its balance sheet of bond holdings by redeeming a portion of its Treasury securities rather than purchasing Treasuries, as it did prior to 2022. Along with the Fed’s reduced role in Treasury purchases, foreign buyers also play a diminished role. “China is less likely to expand its Treasury holdings if it doesn’t have as many dollars to invest based on reduced U.S. trade, and Japan is focused more on internally funding its own debt,” says Haworth. As a result, individual investors, either through direct purchases or via mutual funds, have taken on a much larger role as Treasury debt purchasers.