The early August market downturn was a signal that investors feel the Fed needs to act soon to reverse its recent interest rate policy. Markets anticipate that the Fed will cut rates beginning at its mid-September 2024 meeting, perhaps by as much as 0.50%.6 “After its July meeting, the Fed in its statement put more emphasis on being sensitive to changes in the labor market, when before they were almost totally focused on inflation data,” says Merz. “If the Fed continues to see a modest deceleration in inflation, but balances that with concerns about a decelerating labor market, it gives them more room to cut rates faster than they initially planned.” Merz says investors may see, in the coming months, potentially meaningful Fed rate cuts designed to help keep the economy expanding.

Can the economy stay on track?

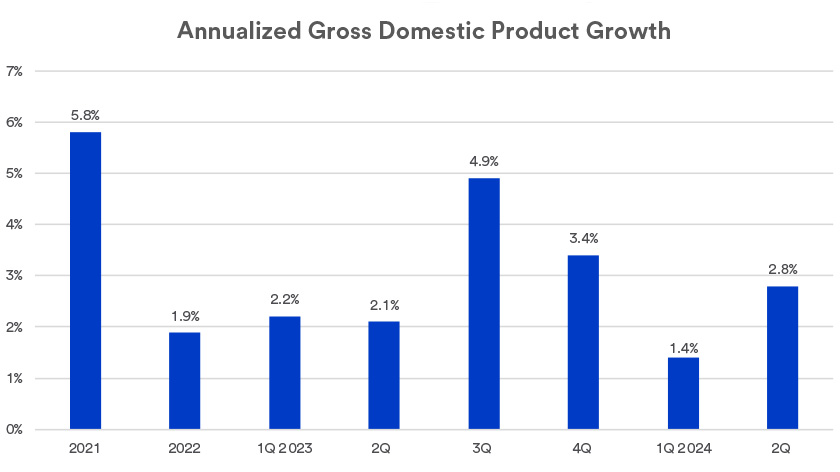

“Modest, steady economic activity continues to be the path we appear to be on at this point, and there don’t seem to be signs of serious recession risk,” says Haworth. “Nevertheless, a big question that may drive the markets and the timing of Fed rate cuts is whether consumers can continue spending at a sufficient pace to keep the economy growing.”

Economic obstacles could still emerge, even as the Fed contemplates initiating rate cuts. “What surveys are telling us is that price levels are challenging for some consumers, and on top of that, borrowing is expensive as well,” says Haworth. “While that may ultimately impact consumer spending levels, we’re not seeing it yet.”

Stubbornly high interest rates complicate matters for businesses as well, particularly as it relates to business capital investment. “If rates stay elevated and companies are forced to issue debt with more significant financing costs, that could dampen business activity and threaten current expectations for economic growth,” according to Haworth. Nevertheless, corporate capital expenditures remain solid to this point.

Implications for investors

“We still think this is a positive investment environment,” says Freedman. “This is a well-telegraphed, slowing economy. If we felt there was a structural economic shift underway, we’d come to a different conclusion.” Freedman says consumers remain in a solid position to play a pivotal role in keeping the economic expansion intact.

Haworth says the combination of ongoing economic growth and persistent inflation make stocks more attractive relative to bonds. Haworth adds if the economy manages to demonstrate ongoing strength in the coming months, that could work to benefit non-technology sectors of the market that are more dependent on favorable economic trends. For example, utility stocks, which struggled in 2023, represent one of the top performing sectors within the S&P 500 year-to-date in 2024.7

Consider reviewing your current portfolio with your wealth management professional to determine if it’s consistent with your long-term goals and positioned to meet the challenges of what continues to be a dynamic market and economic environment.

Note: Diversification and asset allocation do not guarantee returns or protect against losses. The Standard & Poor’s 500 Index (S&P 500) consists of 500 widely traded stocks that are considered to represent the performance of the U.S. stock market in general. The S&P 500 is an unmanaged index of stocks. It is not possible to invest directly in the index. Past performance is no guarantee of future results.