The U.S. job market showed signs of weakness in July, with the growth of new jobs slowing and the unemployment rate ticking higher. In addition, Americans filing new unemployment claims also rose at the end of the month. In early August, investors appeared to read this flurry of softer labor market data as an economy warning sign, with equity markets suffering significant declines.

The latest jobs data arrived just after the Federal Reserve voted to hold interest rates steady, maintaining the fed funds target rate at a range of 5.25% to 5.50%, the same level as the past year. The Fed indicated that the door was open to an interest rate cut at its next meeting in mid-September. Investors initial reaction in the wake of jobs data released in early August indicates a fear that the Fed waited too long to initiate rate cuts.

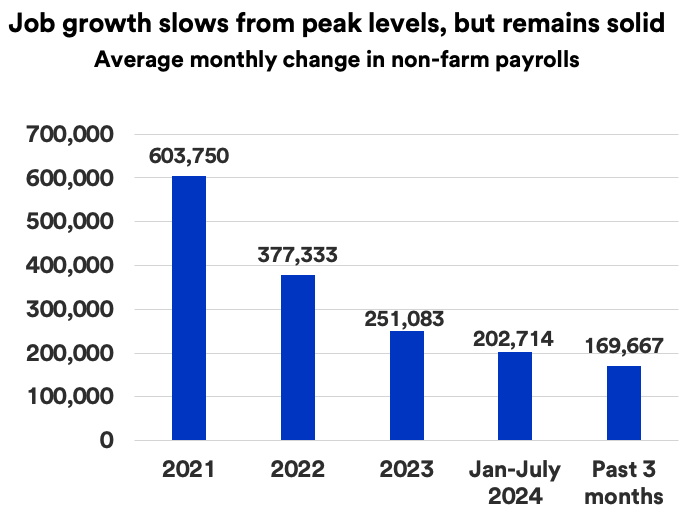

The U.S. Bureau of Labor Statistics reported that the economy created only 114,000 new jobs in July, the second lowest monthly gain in more than four years (behind April 2024when only 108,000 jobs were created). In addition, the labor department revised lower June’s impressive job growth figure. What was initially reported as a 206,000 job gain in June was revised to 179,000. 1

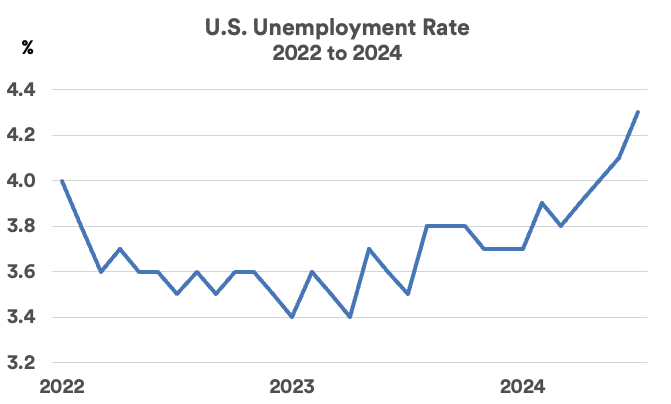

While job growth slowed, the nation’s unemployment rate rose to 4.3%, its highest level since October 2021. 2 “The market’s worry with the unemployment rate is that historically, once it begins rising, it tends to keep rising,” says Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management. “Still, when taking a more historical view of the unemployment rate, a number in the low 4% range is still quite favorable.”