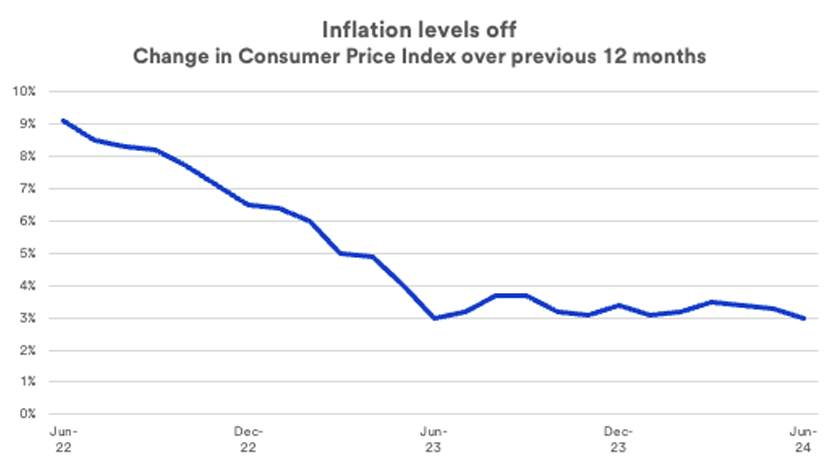

In the meantime, there are other signs that the economy remains on a steady course. It added more than 200,000 jobs in June, and the number of available jobs continue to outpace the number out-of-work Americans looking for a job.4 While Powell indicated the Fed is keeping a close eye on the strength of the labor market as it assesses interest rate policy (maintaining “maximum employment” is part of its mandate), the latest data looks favorable. “There are no red flags right now,” says Rob Haworth, senior investment strategy director for U.S. Bank Wealth Management. “Jobs reports will be closely watched, but lots of data shows us this is still a decent labor market.”

Markets react favorably

Equity and bond markets performed well prior to and following release of the FOMC’s July decision to continue to hold the line on interest rates, at least until September. Stocks, as measured by the benchmark S&P 500 Index, gained more than 1.5% on the day of the Fed’s announcement.5 Bonds rallied as well, with the 10-year Treasury yield dropping to 4.09%, its lowest level since March 2024.6

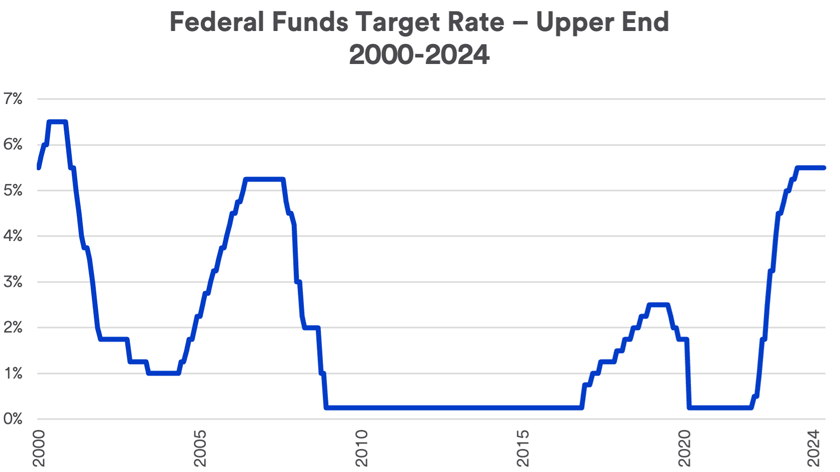

Markets soared early in the year in anticipation that Fed interest rate cuts would begin sooner and happen frequently over the course of the year. However, as it became clear that rate cuts weren’t imminent, markets backtracked. Following a first quarter 2024 gain of more than 10%, the S&P 500 retreated more than 4% in April. Stocks bounced back since, with the S&P 500 up more than 15% through 2024’s first seven months. Similarly, yields on 10-year Treasury bonds, which rose to a peak of 4.70% in April, have declined now to 4.09% at July’s close as investors anticipate pending fed funds target rate cuts.

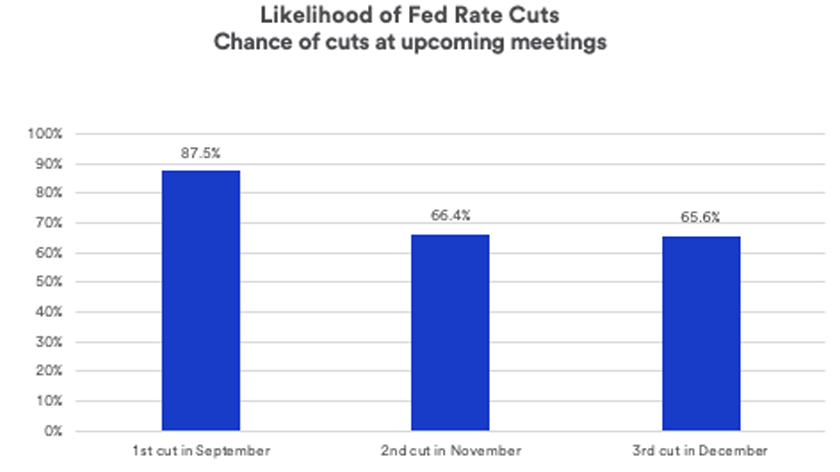

How many Fed rate cuts in 2024?

The CME FedWatch Tool, which analyzes the probabilities of fed fund rate changes based on interest rate trader actions, indicates a high likelihood that the first Fed interest rate cut, of 0.25%, will occur at the FOMC’s September meeting. A smaller majority of these traders anticipate a second rate cut at the November meeting, and an additional cut in December.1 Note, however, that unexpected changes to economic data could rapidly alter this outlook.