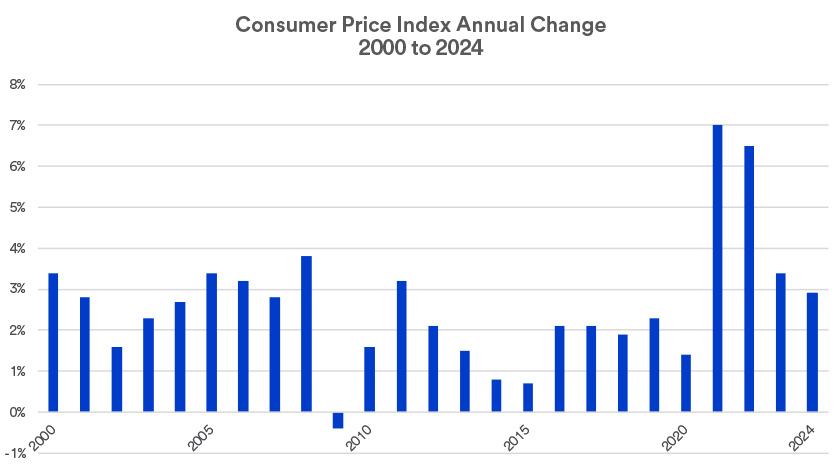

Along with favorable CPI news, there continue to be encouraging developments at the wholesale price level. The main measure of changes to wholesale costs, the Producer Price Index, is up 2.2% over the past year and only 1.2% on a three-month annualized basis, as of July 2024.

Bond market impact

Bond yields, over long-term periods, tend to track the direction of inflation rates. Much of this may be related to Fed monetary policy responding to inflation trends. Since the Fed raised short-term interest rates, bond yields rose commensurately across the board. The benchmark 10-year U.S. Treasury note stood at 4.98% on October 18, 2023 then fell below 4% in late December as investors began to anticipate Fed rate cuts. For much of 2024, 10-year Treasury yields remained firmly above 4%, topping out at 4.70% in April as investors realized that Fed interest rate cuts weren’t on the immediate horizon. However, in early August, amid growing market confidence that the Fed will soon begin cutting rates, 10-year Treasury yields dropped below 4%. “The markets initially anticipated an early start to Fed rate cuts in 2024,” says Haworth. “Nevertheless, markets appear to believe that the Fed is on track to temper inflation, even if it takes a little longer than initially expected,” says Haworth.

How inflation can impact your portfolio

At a time when inflation began to slow from its peak in mid-2022, stocks performed better. In 2024, the S&P 500 has repeatedly reached record highs, though markets recently experienced more volatility. The bond market continues to offer attractive yields for long-term investors. Although yields on some shorter-term securities exceed yields of some longer-term bonds, Haworth says investors should consider placing more emphasis on their ultimate portfolio goals. “It may be an appropriate time to move money out of short-term vehicles and focus on positioning your portfolio in assets, such as stocks and longer-term bonds, that can help you achieve your ultimate financial objectives in the years to come.”

“We still think this is a grind-it-out, improving landscape for investors,” says Freedman. “Corporate profits are still intact and corporate spending remains robust.”

Haworth notes that the stock market has been on an upswing since late 2022. “In general, stock markets can perform well in either a high or low-rate environment, but it is periods of transition from one environment to the next that can cause more significant price swings.”

Haworth says the persistent inflationary environment creates challenges for bond investors. As a result, U.S. Bank’s Asset Management Group currently recommends investors tilt portfolios toward equities, with less emphasis on traditional fixed income.

Generally, a consistent long-term strategy tends to work to the benefit of most investors. This likely precludes any dramatic changes to your asset allocation strategy in response to today’s inflation environment.

Be sure to talk with your financial professional about what steps may be most appropriate for your situation.