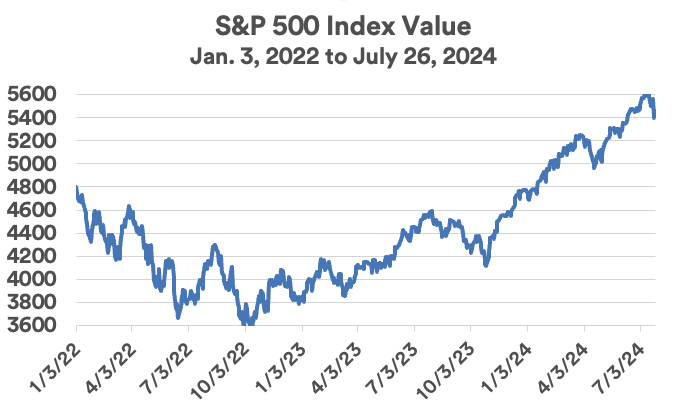

U.S. economy boosts stocks

While interest rate trends can influence the stock market, recent performance appears to be more closely tied to the strength of the U.S. economy. “As the Fed raises interest rates, we typically expect slower economic growth,” says Eric Freedman, chief investment officer for U.S. Bank Wealth Management. Surprisingly, however, U.S. gross domestic product (GDP) grew more quickly in 2023 (2.5%) than it did in 2022 (1.9%). Growth slowed modestly to an annualized 1.4% rate in 2024’s first quarter, but gained momentum in the second quarter, growing at an annualized 2.8% pace.4 “Consumer spending and business capital expenditures remain strong, and that’s a reason for bullishness about stocks in the near term,” says Freedman. He notes that businesses appear committed to getting “bigger, stronger and faster through technology spending,” much of it centered on artificial intelligence applications. That’s provided a solid boost to technology-oriented stocks.

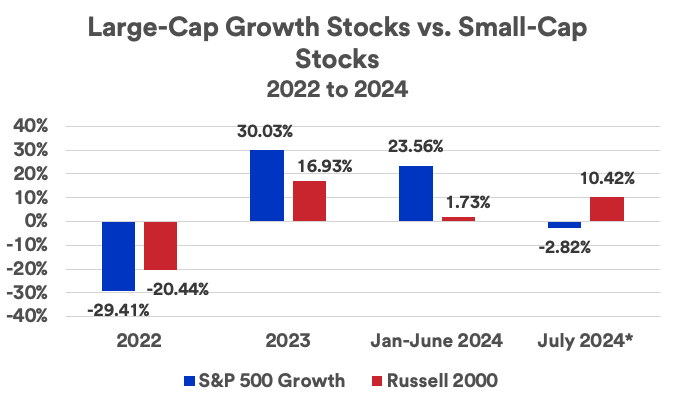

Yet, interest rates are still a consideration for equity investors. Stock prices tended to track with bond yield trends over the course of 2023 and 2024. When interest rates rose, stock prices retreated, and when rates fell, stocks reacted favorably. Haworth says the recent rally in small-cap stocks reflects the market’s anticipation of Fed rate cuts and continued favorable trends in the direction of long-term interest rates.