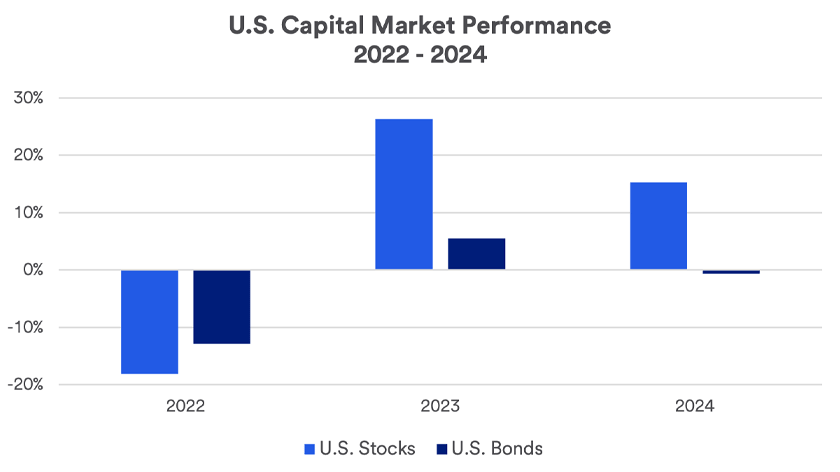

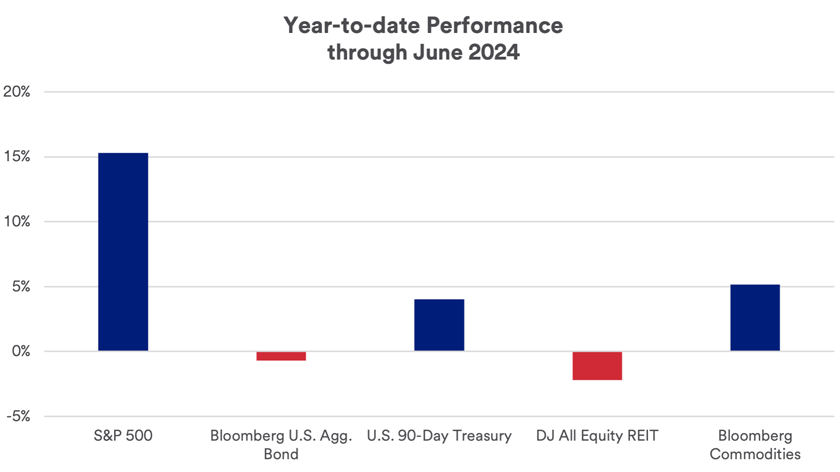

“If we look at the first half of 2024 for equities, the story is all about technology stocks,” says Rob Haworth, senior investment strategy director at U.S. Bank. “Recent advancements in artificial intelligence have spurred corporate investment in technology, and stocks in the technology sector benefited the most as a result.” By contrast, he says, “bond markets faced more challenges related to the fact that the Federal Reserve is holding interest rates higher for longer.” Bonds were down modestly year-to-date through June 30, 2024.

There may be opportunities to make minor yet important adjustments to the broader, long-term positions represented in your portfolio. However, you should pursue such short-term tactical moves carefully.

“Specific tactical moves designed to capture a market opportunity within any of those asset classes require investors to be nimble and willing to move quickly in and out of specific positions,” says Haworth.

Opportunities for tactical asset allocation in today’s environment

- Large U.S. stocks: If you invest in equities, you may want to consider a modest tilt toward stocks over bonds. Since a standard index fund features overweight positions in the largest stocks that have already earned outsized returns, you should consider a fund that offers equal-weight exposure to large U.S. stocks. The largest corporations are less sensitive to interest rates, as many of them extended debt maturities and locked in low interest rates for longer terms before the Fed’s interest rate policy change. These companies also tend to have large cash balances, which are currently earning more than 5% interest. “Smaller companies that are more reliant on refinancing debt may see less earnings growth because borrowing expenses are higher,” Haworth says. As a result, small stock performance has lagged that of large-cap stocks.

- Non-government-agency-backed residential mortgage bonds: Non-taxable fixed-income investors may want to consider residential mortgage-backed securities (MBS) not backed by the government, which have strong fundamentals and offer competitive current income. “These securities are particularly attractive given low mortgage loan balances relative to home values and strong incentives for homeowners to remain current on low fixed-rate mortgages they locked in prior to the onset of higher interest rates,” says Haworth.

- Municipal bonds: Tax-aware investors can earn extra potential returns by slightly extending maturity profiles in municipal bond holdings and incorporating a modest allocation to high-yield municipal bonds. While these are on the riskier end of the tax-free bond spectrum, Haworth notes that “high yield municipal bonds tend to have lower default rates than we see in the corporate high-yield market.”

- Insurance-linked securities: Tied to the sale of reinsurance products, these securities can offer highly competitive income streams in the current environment for certain types of investors, particularly within trust portfolios. “As the cost of insurance has gone up, it has resulted in higher yields for investors in insurance-linked securities,” Haworth says.

Dollar-cost averaging

The second situational strategy is dollar-cost averaging. As you accumulate cash in your portfolio through interest, dividends or security or business sales proceeds, investing this cash into asset classes with higher returns, such as equities, is key to meeting your long-term financial goals. However, market volatility might affect your willingness to put lump sums to work in assets that are subject to fluctuation.

Dollar-cost averaging may increase your comfort level with equity investing during volatile times. This strategy involves investing a portion of your cash balance into the target equity portfolio at regular intervals, rather than trying to invest the cash all at once (a practice called lump-sum investing).

“Dollar-cost averaging is a way to get money invested without experiencing the regret that would occur if markets declined immediately after investing a lump sum,” says Haworth. “It elongates your investment period, so you don’t start at just one price point in the market.”

He says investors holding significant cash sums that are intended to meet longer-term goals should consider putting that cash to work in investments like equities.

“Interest rates are likely to come down at some point in the future,” he says, “so investors can’t count on consistently earning the high yields on cash-equivalent vehicles as they are today.”

Portfolio rebalancing

The third situational strategy addresses the fact that asset prices can move in different directions and at different speeds, and these return variations can cause your initial portfolio allocations to drift from your long-term strategy. Rebalancing your portfolio from time to time may therefore be a good idea depending on your investment objectives.

You should pay particular attention to fixed-income (bond) portfolios if your portfolio emphasized high-yielding, short-term debt securities until now.

“Prior to 2023, investors were dealing with interest rates that were still rising, a riskier environment for long-term bond investments,” says Haworth. “We appear to be at a point where short-term interest rates are near a peak. This may be a time for investors to direct cash-oriented investments into other long-term assets.”