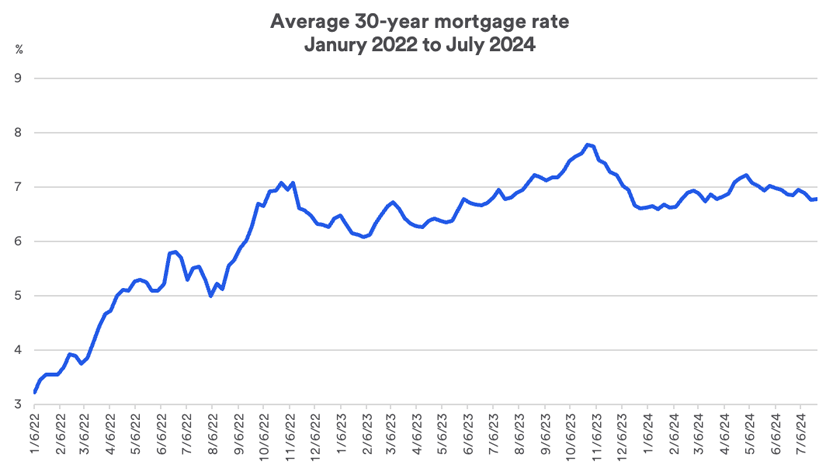

Potential homebuyers appear to be stepping away from the market. For all of 2023, mortgage applications for home purchases fell to their lowest levels since 1995. The challenges remain evident. In late July 2024, the unadjusted Purchase Index for mortgage applications was 15% lower than the same week a year earlier.7

The slowdown in mortgage application activity may reflect the reality facing potential homebuyers hit by a double-whammy of rising prices and elevated mortgage rates. According to the residential real estate brokerage firm Redfin, the median monthly mortgage payment in June 2024 (based on average 30-year mortgage rates and home prices) was $2,671, only slightly lower than the recent all-time high. It still represents a 4.6% increase in the median mortgage payment from one year prior.8 “Housing affordability remains a meaningful problem,” says Haworth. “Potential homebuyers are being priced out of the market, or they need to save up more to make a larger down payment to keep their mortgage payment reasonable.” Haworth says this could lead to some belt-tightening by consumers, which may slow activity in other parts of the economy.

Impact on real estate investing

For those looking to enhance portfolio diversification by including real estate in their asset mix, a commonly used vehicle is a real estate investment trust (REIT). However, as is the case with the housing market, higher interest rates also create headwinds for REITs.

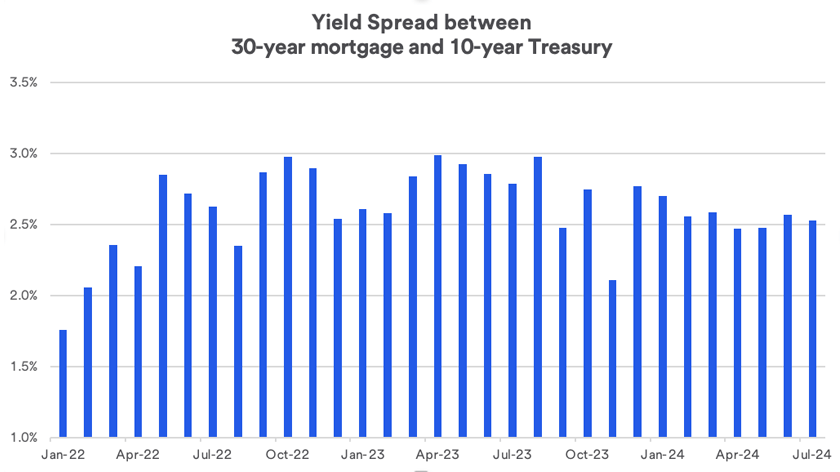

“Although REITs are often considered a way to hedge the risk of higher inflation, the unfavorable interest rate environment has resulted in REITs underperforming other parts of the equity market,” says Tom Hainlin, national investment strategist at U.S. Bank Wealth Management. “Improved yields on U.S. Treasury securities create cash flows that look much more attractive in today’s market when compared to REITs.” As a result, demand for REITs has fallen. Year-to-date through July 29, 2024, the S&P Developed REIT index gained 3.55%, compared to a year-to-date total return of 15.44% for the broader S&P 500. Over the 12-months ending July 29, 2024, the S&P 500 gained 21.02% while the Developed REIT index was up just 9.13%.9

Haworth says REIT valuations recently declined to a low enough point to entice more investor interest. “Yet there remain serious challenges in the commercial real estate market, and those are likely to impact REIT values as well.”

Housing’s economic influence

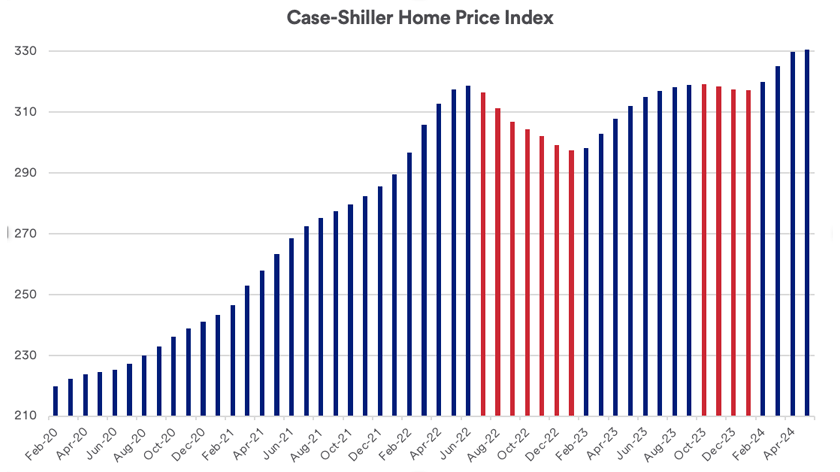

Fed policy has clearly placed housing and other real estate markets on the front lines of efforts to slow the economy's pace and lower inflation. Thus, regardless of the extent of your real estate holdings, it’s important to keep in mind that the housing market can have a significant impact on the broader economy and capital markets generally. “The formation of households is one of the main drivers of economic growth in the U.S.,” says Hainlin. “It has a large spillover effect on the economy, including materials that go into building or remodeling, and furnishings for homes.”

Be sure to consult with your wealth management professional to determine when and how real estate investments might be a good fit for you.