With deadlines fast approaching, Congress acted in late May and early June 2023 to temporarily suspend the federal government’s debt ceiling. Both houses of Congress passed the Fiscal Responsibility Act of 2023. This action avoided the possibility of a government default, allowing the U.S. Department of the Treasury to continue issuing debt to meet the federal government’s fiscal needs. The bill suspends the debt ceiling until January 1, 2025, then increases the limit shortly thereafter to accommodate debt obligations issued during the suspension period.

The debt ceiling requires frequent adjustments to allow the federal government to continue to borrow to pay its obligations. The issue drew more attention after the government reached its debt limit in January 2023. However, the impact on capital markets was generally limited, notwithstanding dire warnings of serious economic consequences should the government default. This reflected investor confidence, despite partisan disagreements, that Congress would resolve the issue in time to avoid a default, as they have in the past.

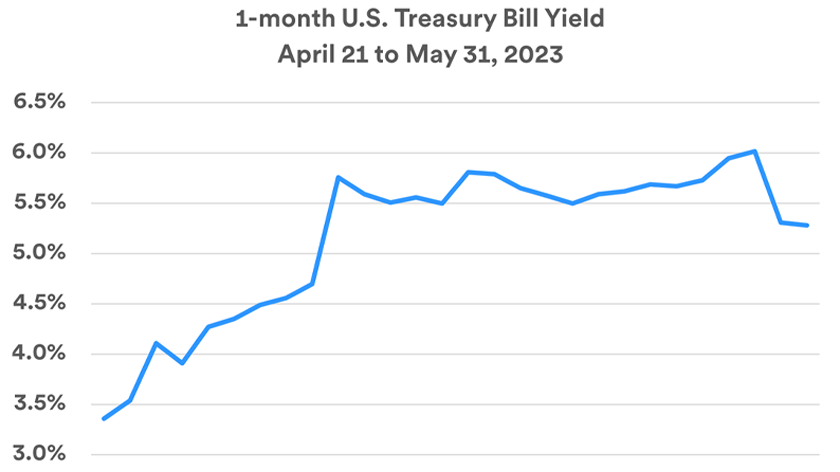

While the debt ceiling issue was regularly in the headlines over the first five months of 2023, it appeared to do little to move the stock market. During that time, the value of the benchmark S&P 500 index fluctuated between 3,800 and 4,200. There was more apparent impact in the bond market, particularly in short-term U.S. Treasury securities, where yields moved higher. This movement reflected investor concerns about the increasing risk of political gridlock over the debt ceiling issue. “Markets witnessed battles over the debt ceiling before, and always saw the situation resolved in a timely manner. The expectations were that this would happen again,” says Rob Haworth, senior investment strategy director at U.S. Bank.

What is the debt ceiling?

The federal debt is the total amount of money the government owes for spending on everything from Social Security and Medicare to defense programs and other types of domestic and overseas expenditures. The debt limit set by Congress represents the funds that the U.S. Treasury is authorized to raise through debt security offerings to pay the government’s operating costs.

Although it’s a somewhat arcane procedure, raising the debt ceiling allows the U.S. Treasury to continue debt issuance to pay for Congressionally approved federal government spending. “Increasing or suspending the debt limit does not authorize new spending commitments or cost taxpayers money,” explains Treasury Secretary Janet Yellen. “It simply allows the government to finance existing legal obligations that Congresses and Presidents of both parties have made in the past.”1

The need for such Congressional action has occurred nearly one hundred times since World War II. Most often, passage is a routine piece of business for legislators, but in some years, it becomes more of a political issue.

How the issue was resolved

Republican leadership in the House made clear that it was not willing approve a “clean” debt ceiling increase sought by President Biden. Rather, they proposed spending cuts as part of an agreement to increase the government’s borrowing powers. On April 26, 2023, the Republican-controlled U.S. House narrowly passed a bill extending the debt ceiling but included a plan for cuts to discretionary domestic spending programs. The legislation, titled the Limit, Save and Grow Act called for extending the debt limit for less than one year. President Biden and other Democrats generally opposed this effort.

Passage of the Republican-sponsored bill opened the door for serious negotiations between leaders of both parties. In late May, President Biden and House Speaker Kevin McCarthy announced terms of a debt ceiling extension agreement that also addressed a range of budgetary issues. This agreement led to the Fiscal Responsibility Act of 2023. The House approved the package by a large margin with significant votes from both parties. The bill then moved onto the Senate, which after voting down a wide range of amendments, eventually approved the bill based on the Biden-McCarthy agreement.

Here are some key provisions of the Fiscal Responsibility Act of 2023.

Suspension of the debt ceiling

The federal debt limit that was the primary focus of the package, was suspended through January 1, 2025. Then, the debt limit will be increased on January 2, 2025, to accommodate obligations issued during the suspension period. Notably, it means Congress will not need to address this issue prior to the 2024 elections.

Discretionary spending cap

The agreement includes a provision to maintain “roughly flat” non-defense discretionary spending levels in 2024, with only a 1% increase allowed in 2025.

Defense spending boost

Terms include an increase of roughly 3% in total defense spending in 2024, to $886 billion. This is in line with President Biden’s spending proposal. It also provides funding for the Department of Veterans Affairs Cost of War Toxic Exposure Fund.

Reduced Internal Revenue Service (IRS) funding

An additional $80 billion previously appropriated to the IRS to update its systems and enhance tax code enforcement was reduced by $20 billion.

“Clawback” of unused COVID relief funds

Unspent dollars provided for relief programs related to the COVID-19 pandemic will be returned. This is estimated to total $50 to $70 billion.

Work requirements for government support programs

The new legislation expands the number of low-income individuals who must meet work requirements to qualify for food assistance programs. The top age at which the work requirement applies will rise from 49 to 54.

Changes to student loans

Payments on federal student loans were suspended at the beginning of the COVID-19 pandemic. The legislation requires the Biden administration to lift the suspension on federal student loan repayments by August 30, 2023.

Expedited energy permitting process

Stipulations are included to ease the process of obtaining permit approvals for new energy projects. This includes fossil fuel-based projects as well as green energy initiatives.

Some perspective on the debt ceiling debate

This repeated and ongoing issue added a degree of stress to capital markets in the first half of 2023, even with Congress’ track record of ultimately voting to raise the debt ceiling. “As long as the issue lingered, there was always a question of what it might mean for the economy and capital markets,” says Haworth. However, he is skeptical that settlement of the issue is the key to a sustainable stock market rally. “It removes a risk to the markets, but it is unlikely to be a catalyst for change to fundamental factors like corporate earnings, for example, that will likely impact stock prices over the course of 2023 and beyond,” according to Haworth.