Webinar

Summer 2024 Investment Outlook – July 23 Replay

Is the growth momentum sustainable?

July 1, 2024

The year’s second half brings significant events alongside the usual capital market cacophony: The U.S. campaign season alongside elections in several key countries, NATO and G20 summits, the Olympics and other major developments set to unfold. The Federal Reserve (Fed) and other central banks remain in focus as investors anticipate a transition from officials raising interest rates to cutting rates. Businesses and consumers continue to show strength, with some divergence under the surface at the country, sector and income distribution levels, requiring investors to anticipate marginal change. While the global economy is expected to slow, the growth impulse remains positive and corporate earnings continue to deliver despite high expectations.

Asset classes had mixed performance to start 2024, with global equities providing positive total returns led by the United States and followed by emerging markets and developed international. Bonds remain more sluggish due to sticky inflation pressures impacting prices, which has helped commodities thus far in 2024. Real Estate stocks have been underwhelming to kick off the year, with income offset by weaker prices as investors weigh how much further repricing may exist across office, multifamily and other property market subsectors.

We continue to hold a positive forward outlook for diversified portfolios. Our bias has been to favor equities and real assets over fixed income; we remain optimistic on consumer and business spending with companies continuing to prioritize shareholders through stock buybacks and dividends. Inflation will likely gradually recede but remain pesky, and investors could seek inflation protection in portfolios through commodities. We do see several opportunities for bond investors across both taxable and tax-exempt fixed income, but we emphasize diversified yield sources.

While we maintain a constructive forward view, we are mindful of election risks, commercial real estate woes, ongoing geopolitical tensions, potential consumer and business deceleration that exceeds expectations, and other variables that could drive adverse capital market activity. Our process remains team oriented, global in scope and data driven. We appreciate the opportunity to share views across the capital market landscape through our team-based approach.

― Eric Freedman, Chief Investment Officer, U.S. Bank

Quick take: The U.S. economy remained solid in 2024’s first half with strong growth, moderating inflation and a tight labor market. Developed market economies are delivering a modest recovery as global central banks begin to trim interest rates. Emerging market economic growth is diverse; China is struggling to reignite activity, India remains resilient and regional Asian economies are benefiting from technology infrastructure spending.

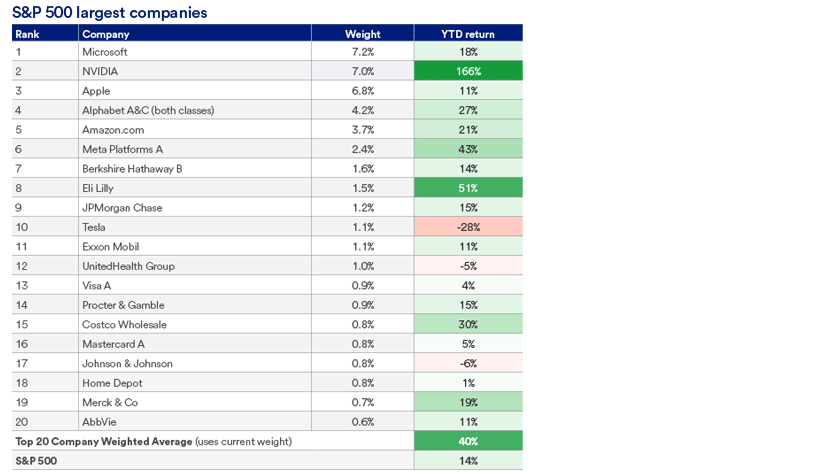

Quick take: AI enthusiasm continues to push broad U.S. equity indices higher in 2024. Decelerating inflation, moderating interest rates and stable earnings growth are directionally consistent with higher equity prices.

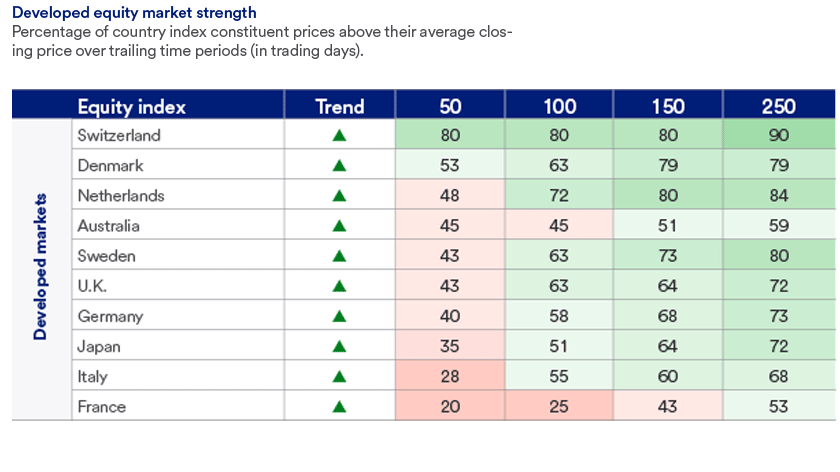

Quick take: Policy support remains a key variable driving foreign developed equity returns, while broadening sector and constituent company participation highlight positive market momentum heading into 2024’s second half. Idiosyncratic return drivers lead to a mixed outlook across emerging market equities.

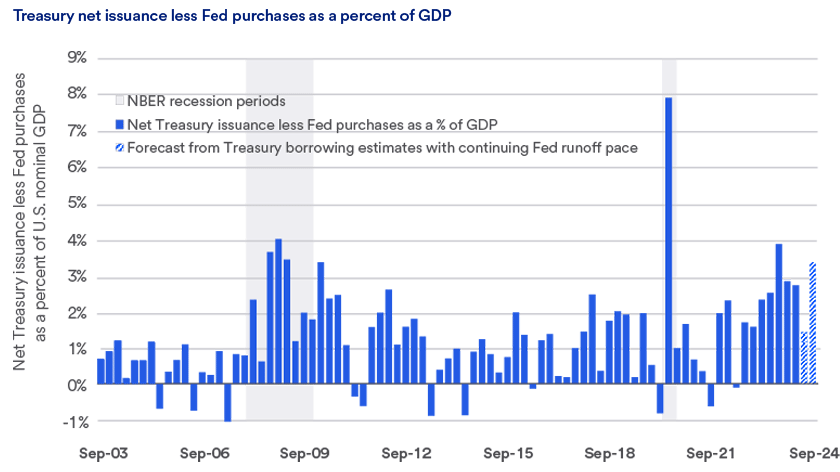

Quick take: High-quality bonds offer compelling yields, but inflation remains a lingering risk for bond prices. Supplementing high-quality bond allocations with riskier high yield bonds and unique fixed income exposures like non-agency mortgages and insurance-linked securities (reinsurance) can boost and diversify portfolio income.

Quick take: Publicly traded real estate investment trusts (REITs) are poised to generate solid returns should interest rates fall. Additionally, increased capital expenditures to power AI and “green” energy should benefit infrastructure companies and commodities.

Quick take: Hedge fund managers are positioning for opportunities amid geopolitical and macroeconomic volatility, with this year’s historic national elections covering half of the world’s population creating additional uncertainty. Tactically oriented managers who stay nimble and can trade quickly appear well suited for this environment.

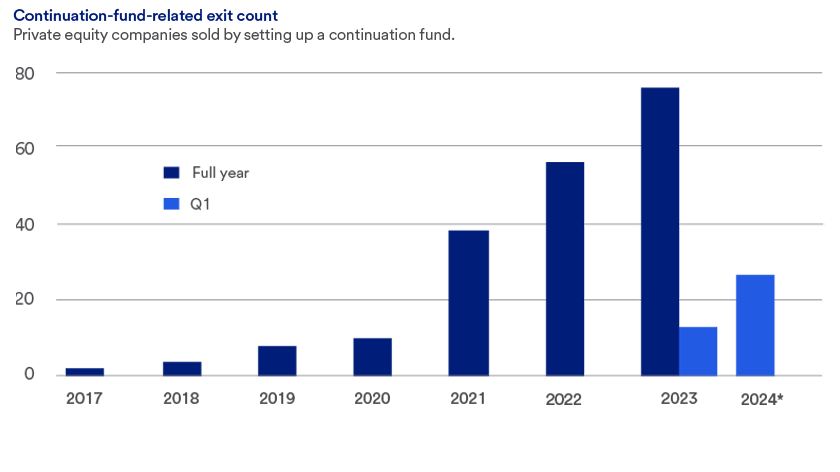

Quick take: Private equity investment managers continue to drive value by acquiring smaller businesses to build up their existing portfolio companies in fragmented industries. Investment managers are also actively acquiring corporate carveouts, identifying opportunities to implement value creation strategies on these often-undermanaged subsidiaries of larger companies.

This commentary was prepared June 2024 and represents the opinion of U.S. Bank. The views are subject to change at any time based on market or other conditions and are not intended to be a forecast of future events or guarantee of future results and are not intended to provide specific advice or to be construed as an offering of securities or recommendation to invest. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Not a representation or solicitation or an offer to sell/buy any security. Investors should consult with their investment professional for advice concerning their particular situation. The factual information provided has been obtained from sources believed to be reliable but is not guaranteed as to accuracy or completeness. Any organizations mentioned in this commentary are not affiliated or associated with U.S. Bank in any way.

U.S. Bank and its representatives do not provide tax or legal advice. Your tax and financial situation is unique. You should consult your tax and/or legal advisor for advice and information concerning your particular situation.

Diversification and asset allocation do not guarantee returns or protect against losses. Based on our strategic approach to creating diversified portfolios, guidelines are in place concerning the construction of portfolios and how investments should be allocated to specific asset classes based on client goals, objectives and tolerance for risk. Not all recommended asset classes will be suitable for every portfolio.

Past performance is no guarantee of future results. All performance data, while deemed obtained from reliable sources, are not guaranteed for accuracy. Indexes shown are unmanaged and are not available for investment. The S&P 500 Index is an unmanaged, capitalization-weighted index of 500 widely traded stocks that are considered to represent the performance of the stock market in general. The Consumer Price Index is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care. It is one of the most frequently used statistics for identifying periods of inflation or deflation.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible difference in financial standards and other risks associated with future political and economic developments. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility. Investing in fixed income securities is subject to various risks, including changes in interest rates, credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Investments in debt securities typically decrease in value when interest rates rise. The risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher-rated securities. Investments in high yield bonds offer the potential for high current income and attractive total return but involve certain risks. Changes in economic conditions or other circumstances may adversely affect a bond issuer’s ability to make principal and interest payments. The municipal bond market is volatile and can be significantly affected by adverse tax, legislative or political changes and the financial condition of the issuers of municipal securities. Interest rate increases can cause the price of a bond to decrease. Income on municipal bonds is free from federal taxes but may be subject to the federal alternative minimum tax (AMT), state and local taxes. There are special risks associated with investments in real assets such as commodities and real estate securities. For commodities, risks may include market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors. Investments in real estate securities can be subject to fluctuations in the value of the underlying properties, the effect of economic conditions on real estate values, changes in interest rates and risks related to renting properties (such as rental defaults). Hedge funds are speculative and involve a high degree of risk. An investment in a hedge fund involves a substantially more complicated set of risk factors than traditional investments in stocks or bonds, including the risks of using derivatives, leverage and short sales, which can magnify potential losses or gains. Restrictions exist on the ability to redeem or transfer interests in a fund. Private capital investment funds are speculative and involve a higher degree of risk. These investments usually involve a substantially more complicated set of investment strategies than traditional investments in stocks or bonds, including the risks of using derivatives, leverage, and short sales, which can magnify potential losses or gains. Always refer to a Fund’s most current offering documents for a more thorough discussion of risks and other specific characteristics associated with investing in private capital and impact investment funds. Reinsurance allocations made to insurance-linked securities (ILS) are financial instruments whose performance is determined by insurance loss events primarily driven by weather-related and other natural catastrophes (such as hurricanes and earthquakes). These events are typically low-frequency but high-severity occurrences. Private equity investments provide investors and funds the potential to invest directly into private companies or participate in buyouts of public companies that result in a delisting of the public equity. Investors considering an investment in private equity must be fully aware that these investments are illiquid by nature, typically represent a long-term binding commitment and are not readily marketable. The valuation procedures for these holdings are often subjective in nature. Private debt investments may be either direct or indirect and are subject to significant risks, including the possibility of default, limited liquidity and the infrequent availability of independent credit ratings for private companies.

Knowing your investment goals and risk tolerance helps us diversify your portfolio with a mix of equities, bonds and real assets.

January 6, 2023

Learn what new tax law changes included in the Inflation Reduction Act and SECURE Act 2.0 may mean for you.

After a dip in April, the S&P 500 and other major stock market indices continue to rally, hitting historic highs.