Key takeaways

Cash and cash equivalents can provide liquidity, portfolio stability and emergency funds.

Cash equivalent securities include savings, checking and money market accounts, and short-term investments.

A general rule of thumb is that cash and cash equivalents should comprise between 2% and 10% of your portfolio.

Cash and cash equivalents play a variety of roles in your investment portfolio and financial plan, including providing liquidity, portfolio stability and emergency funds for unexpected events. Cash equivalent vehicles are typically defined as money held in different types of accounts, such as savings, checking and money markets, as well as short-term investments with maturities less than 90 days, such as CDs, bonds and Treasuries.

“Laddering cash equivalents into short-, mid- and longer-term investment vehicles is very important because it provides liquidity and backup and is a good way to diversify your fixed-income portfolio.”

D.J. Verhaalen, Wealth Management Advisor for U.S. Bancorp Investments

The proper role for cash in a portfolio is determined in part by your risk tolerance and your current stage in life. For retirees who are no longer generating a paycheck, cash can help provide peace of mind that they have sufficient liquid reserves to weather periods of uncertainty or a downturn in the economy.

For investors who are willing to take on more risk, cash and cash equivalents also offer liquidity that can allow them to move quickly to take advantage of investment opportunities, particularly when there is disruption or fluctuation in the market.

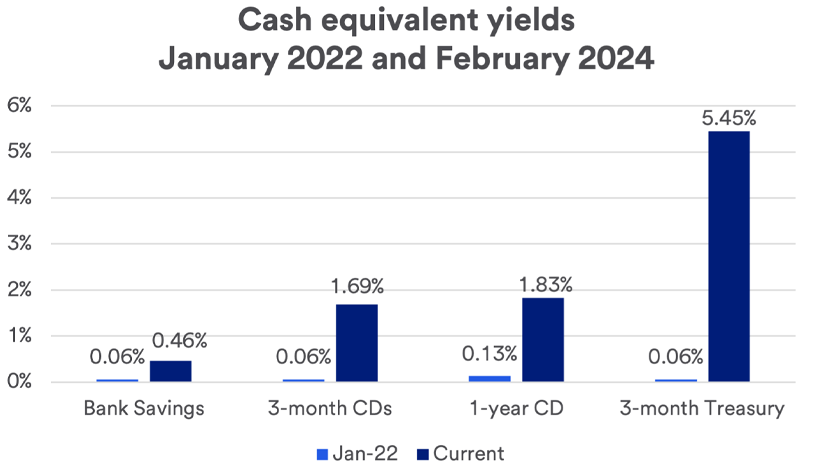

What can I expect to earn on cash and cash-equivalent investments?

Today’s interest rate environment is dramatically changed from what existed just a few years ago. This creates an opportunity to enhance your overall portfolio results. “A first step is to move cash into short-term instruments that pay more attractive yields given today’s interest rates,” says Haworth.

How much cash should I have in my portfolio?

Determining the appropriate cash level for your portfolio is a common question, and the answer varies depending on your unique circumstances and current market conditions. Some factors that help to determine how much cash and cash equivalents to hold include:

- Your financial goals and objectives

- Your time horizon for investing

- Your spending needs

- Your risk tolerance

A general rule of thumb is that cash or cash equivalents should range from 2% to 10% of your portfolio, although the right answer for you will depend on your individual circumstances.

One situation where extra cash may make more sense is if you’re planning on a big purchase or expense within the next few years, such as buying a home, paying for college tuition or undergoing a major home renovation. On the other hand, some people might maintain a lower cash position based on their leverage opportunities. “In a low-interest rate environment, for example, you might have equity built up in your home that you can tap into, such as through a home equity line of credit, versus holding extra cash,” says D.J. Verhaalen, Wealth Management Advisor for U.S. Bancorp Investments.

Income and net worth are two additional considerations. For example, people with a steady income can often count on liquidity from a paycheck or annual bonus which may allow them to reduce their cash position. Others who work as independent contractors or have jobs where income may vary may want to hold more in cash reserves to protect against an unexpected income shortfall or be prepared for a sudden expense, notes Verhaalen.

Cash and cash equivalents: Weighing the pros & cons

It can be challenging to find the right balance of cash and cash equivalent holdings. A common mistake people make is carrying too much or too little cash for their situation, as well as putting cash in the wrong investments.

As an example, with the market volatility that occurred in 2022 and the allure of higher interest rates that followed, some investors increased their cash positions and reduced stock and bond holdings. But this might have had negative consequences for their overall portfolio. “Despite the elevated yields for cash vehicles, a diversified portfolio of stocks and bonds likely generated superior performance in 2023,” says Haworth. “Historically speaking, a diversified portfolio emphasizing stocks and bonds will outperform cash.”

What are the pros and cons of holding significant cash position in your portfolio? The answer may vary depending on an your situation.

- Maintaining high cash levels in your portfolio: For some people, it’s a matter of personal preference. They may feel more comfortable with a conservative mix of assets. Another advantage of holding a meaningful cash position is that additional liquidity gives you more flexibility to take advantage of new investment opportunities should they arise. The number one drawback of having too much cash is that you may be sacrificing the return potential of investments in stocks and bonds.

- Keeping too little cash in your portfolio: The primary advantage of holding a limited amount of cash is that you have more money available to invest with the goal of earning potentially higher returns with stocks and bonds. On the downside, you don’t have the liquidity to take advantage of new investment opportunities, and you have less of a buffer against periods of negative stock and bond market performance.

The role of cash and cash equivalents in your financial plan

Cash equivalents should be part of a regular discussion about your holistic financial plan. “When we build a financial plan for clients, we tend to be a little bit more conservative, because we believe managing risk is important,” says Verhaalen.

Verhaalen often recommends clients maintain a cash reserve that’s, at a minimum, the equivalent of six months of income. In addition, he’ll run a financial plan to determine an ideal amount of cash to hold based on an individual’s unique circumstances, as well as how to ladder it into different types of cash equivalents depending on the time horizon and when cash might be needed.

- Shorter-term cash needs of 0-6 months should generally be kept in liquid accounts, such as savings, checking, money market accounts or Treasury notes.

- Cash needs between six months and three years can be supported using vehicles such as a 12-month CD or Treasury notes and bonds.

- For funds not needed for at least three-to-five years, longer-term cash equivalents such as CDs, Treasuries or bonds with a fixed maturity should be considered.

“Laddering cash into short-, mid- and longer-term investment vehicles is very important because it provides liquidity and backup and is a good way to diversify your fixed-income portfolio,” says Verhaalen. For example, if your child is going to college, you might decide to set aside cash in a checking or money market account to cover the first semester’s tuition, put the second semester’s tuition in a six-month CD, the following year’s tuition savings in a 12-month CD and so on.

Verhaalen may also recommend that clients ladder cash equivalents in fixed-income assets with maturities on a regular basis, allowing them to reinvest and capture yield as rates go up.

Investors should review the percentage of cash positions in their investment portfolio periodically as part of regular financial plan review. Consider reviewing your financial plan with your financial professional at least annually or more often if circumstances change.

Just as your life evolves, so should your financial plan. Learn how we can help you design a plan that fits your life.

Related articles

How to use liquid asset secured financing for short-term cash flow needs

Leveraging the assets in your investment portfolio through a flexible line of credit can provide quick access to cash.

How sequence of returns risk can impact when to retire

Choosing when to retire is an important financial decision. A retirement income strategy may help protect your plan against sequence of returns risks.