If you’re considering adding hedge funds to your investment portfolio, it’s important to fully understand how hedge funds work, including their specific structure, risks and potential benefits. You’ll also want to consider the range of available investment strategies to make sure they fit within your overall investment strategy and risk tolerance.

What is a hedge fund?

A hedge fund is an investment vehicle that pools money from many individuals and organizations and invests in a wide range of liquid and illiquid securities in the hopes of high returns. They originated in the 1940s when wealthy investors were looking for ways to include assets in their portfolios that did not closely correlate with the performance of traditional investments.

Hedge funds are managed differently from traditional stocks, bonds or mutual funds, so they fall under the category of “alternative investments.” Until recently, hedge funds were only an option for pension plans, large institutions that manage money for individuals or organizations, and clients with millions of dollars to invest. Today, due to interest regulators allowed participation in hedge funds to broaden to include more individual investors.

“Investors may find value in hedge funds,” says Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management. “It’s important that you carefully assess your options and try to find the most appropriate strategy to fit your portfolio.”

It’s important to note that hedge funds are considered a high-risk investment, so investors need ensure they’re comfortable with this risk.

Who can invest in hedge funds?

If you’re considering investing in a hedge fund, you’ll have to meet eligibility requirements, which vary from fund to fund and are guided by the Securities and Exchange Commission. Most notably, individual investors typically must have a high net worth and/or a significant amount of money to invest.

What does a hedge fund manager do?

A hedge fund manager, which can be an individual or a firm, is critical to the success of a hedge fund. They are responsible for the hedge fund’s overall investing strategy and operations.

One of their responsibilities is to allocate the investment dollars they oversee. They have significant flexibility in how they do this, which is why it is so important that they have extensive knowledge and experience.

“Be aware that certain hedge fund managers have a track record that demonstrates the meaningful value they offer,” says Haworth, “but others have not established extensive or competitive track records.”

Ensure that the hedge fund manager you’re considering undertakes sourcing and due diligence processes to choose funds that are likely to meet the stated risk and performance targets. They should also identify funds that are well-suited for their clients’ goals and constraints. This requires significant industry knowledge, resources and time, because managers must constantly monitor hedge fund launches and closures.

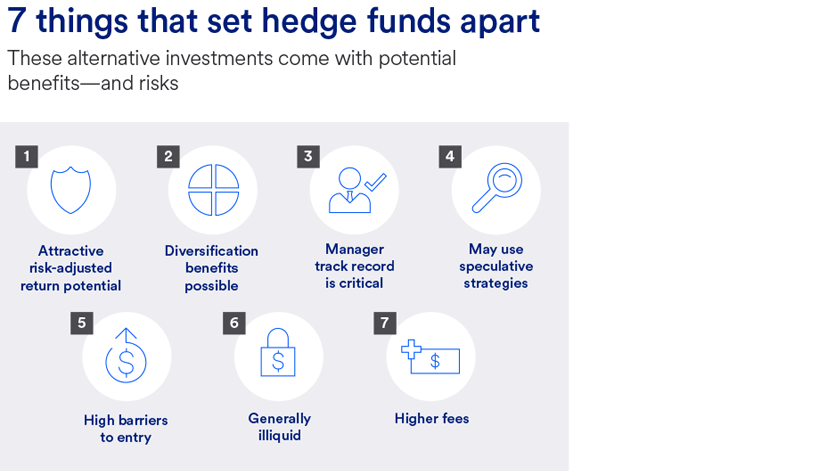

What are the potential benefits of hedge funds?

Because hedge funds are managed differently than traditional mutual funds, there are a few potential benefits to note.