Bonds are available in many forms. You can invest directly in individual bonds, including:

- U.S. Treasury securities

- Municipal bonds

- Debt instruments issued by corporations

- Bonds offered by government entities

- Mortgage-backed securities

- Bonds that originate in overseas markets.

This is where bond diversification is important. Yields will vary based on the credit quality of the issuing entity, the duration of the bond (how long before it matures) and current market conditions. Many investors choose to invest in bond mutual funds, a professionally managed, diversified portfolio of bonds from different issuers.

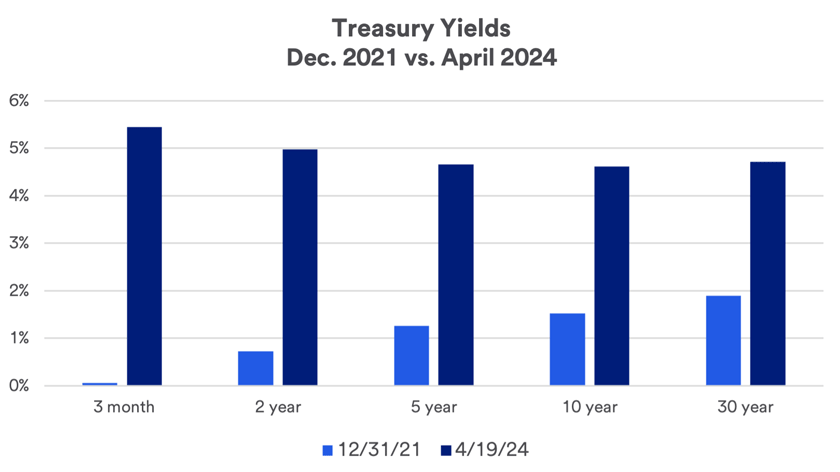

“In a period such as today, when the economy remains strong, investors should feel more comfortable taking on some marginal risk in their bond portfolio to earn higher yields,” Haworth says. This can include adding more positions in corporate debt securities.

As far as how you receive income from bonds, you receive periodic payments from the bond issuer based on the stated annual yield effective at the time you invest. You can choose to hold the bond to maturity, at which time the issuing entity will repay the principal. Alternatively, you can choose to sell bonds on the open market before maturity.

In this case, the market value of a bond may vary from its face value, depending on the interest rate environment and the remaining bond term.

- If current market rates are higher than an existing bond’s coupon, bond issuers will need to offer bonds at a discount to attract buyers.

- If current interest rates are lower than the bond’s current coupon, the bond will sell at a premium to reflect that difference.

This raises an important point that investors often overlook: Bonds, while often considered a lower-risk investment, can fluctuate in value.

Benefits of bonds:

- A stream of income with potentially competitive yields

- Liquidity that allows flexibility to make timely changes to a portfolio mix

- Access to a wide range of fixed income instruments with different yields and risk characteristics

- The ability to provide effective diversification to help offset risk in a portfolio that includes equities and other asset classes

Challenges of bonds:

- Tax at ordinary income rates on bond income, except for tax-free municipal bonds

- The risk of principal loss should interest rates move higher and the investor needs to sell the bond

- Difficulties generating comparable income in the future when replacing maturing bonds

- Lack of inflation protection as income streams established in a bond portfolio remain consistent

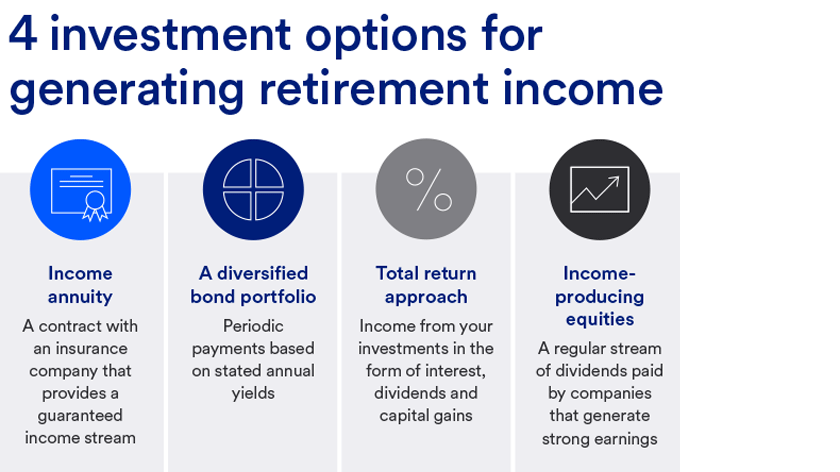

3. Total return investment approach

A total return approach provides income from your investment portfolio in the form of interest, dividends and capital gains. This type of portfolio invests in a diverse mix of stock and bond funds adjusted for your risk tolerance.

In this context, “total” return means you spend a portion of the average annual rate of returns — income and appreciation — over a longer period (10 to 20 years), rather than focusing on specific annual return rates or just drawing income generated by holdings in your portfolio. The aim is that this total return meets or exceeds your withdrawal rate.

“This is a way to grow a retirement portfolio to assure that it continues to meet the needs of people preparing for a retirement that could last 20 to 30 years or longer,” says Haworth. “It may offer a way to generate a superior total return compared with other investment approaches traditionally pursued in retirement.”

Haworth gives the example of 2022, when both stocks and bond suffered declines. “In such an environment, it’s costly to take withdrawals from assets that have suffered a setback,” he says, “because once that money is pulled out, it’s not possible to recoup losses when markets recover.”

This can be particularly challenging early in retirement, depleting assets to a level that potentially puts long-term retirement security at risk.

In terms of withdrawal rate, a total return approach follows a “systematic withdrawal” strategy, in which you take a certain percentage of your investment as a distribution each year. The distribution amount generally ranges between 3% and 5% of the total value of the portfolio.

Benefits of a total return approach:

- It can meet your immediate cash flow needs while continuing to build savings for future expenses, which are likely to rise over time due to inflation.

- It gives you the ability to utilize a broader range of assets than you can do with more typical approaches to retirement income.

- It generates a stream of portfolio withdrawals primarily through by capital appreciation, which is potentially a more tax-efficient form of income.

Challenges of a total return approach:

- There is no guarantee that funds will last throughout retirement.

- The value of your return can vary from year to year (there is no specific withdrawal rate).

- Assets may run out before the end of retirement, particularly in circumstances where investments suffer significant declines in the early years of retirement.

4. Income-producing equities

While people primarily invest in stocks to generate capital appreciation in a portfolio, some equities provide income in the form of dividends. Not all stocks pay dividends, and of those that do, certain stocks tend to pay higher dividends than others.

“Stock dividends became much more attractive when we experienced an extremely low interest-rate environment in the bond market,” Haworth says. “Today, dividend yields of most stocks are not as competitive as bond yields but still offer the potential for capital appreciation.”

Companies typically pay dividends on a quarterly basis. They occasionally pay a “special dividend” due to unusual circumstances, but those are uncommon and not something you should count on. Unlike most bonds, stock dividends can vary with each payout period, and sometimes companies discontinue dividend payments. You need to be prepared for a degree of uncertainty with dividend payouts.

If your primary focus is to invest in a stock for income, it’s important to review its dividend-paying history. Stocks with a reliable history of consistent or steadily increasing dividend payouts are likely to be the most attractive to consider for this purpose. However, depending on the market environment, dividend-paying stocks may not generate total returns comparable to other types of stocks.

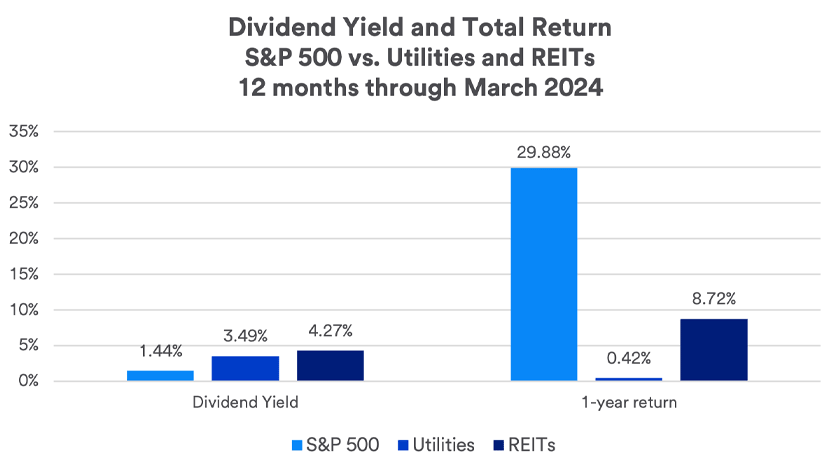

“In recent times, a high proportion of dividend-paying stocks are those that have been most hurt by the current higher interest-rate environment,” Haworth says. These include utilities and real estate investment trusts (REITs).