Long-term care refers to assistance with medical or personal needs over an extended amount of time.

Close to 70% of people turning 65 today will need long-term care at some point in their life,1 making it an issue that touches almost every household. And while many people will be affected by the need for long-term care, not everyone takes advantage of long-term care insurance to help with the costs.

However, long-term care is a considerable expense, and many people can’t afford to cover the entire costs out-of-pocket. Traditional employer-based health insurance won’t cover extended daily care, and in general, health insurance only pays for doctor and hospital bills. Long-term care insurance (LTCI) can help offset the expenses of long-term care needs.

These 7 factors can help you determine whether LTCI is something you should pursue as you plan your financial future.

1. Long-term care insurance covers care in a variety of settings.

When people think of long-term care, most think of nursing homes. However, 73% of people who receive long-term care are at home, not in assisted living facilities or nursing homes.2

Long-term care is needed when someone can’t perform daily activities such as dressing, eating, bathing, or transferring – and this help can often be provided in your own home through a home health aide. Though it’s not necessarily pleasant to think of scenarios where long-term care will be needed, LTCI can help cover the costs. It may offer a way for you to receive care in your own home instead of in an assisted living or nursing home.

2. Long-term care insurance can help fill in caregiving gaps.

It’s impossible to know for sure if your family would be able to care for you if long-term care becomes necessary. Caregiving can be a huge financial and emotional burden. And because of the high cost of long-term care, 66% of caregivers end up using their own retirement and savings funds to pay for care.3 Plus, the logistics of caregiving might not be feasible if your family members live far away or can’t square it with work or family obligations of their own.

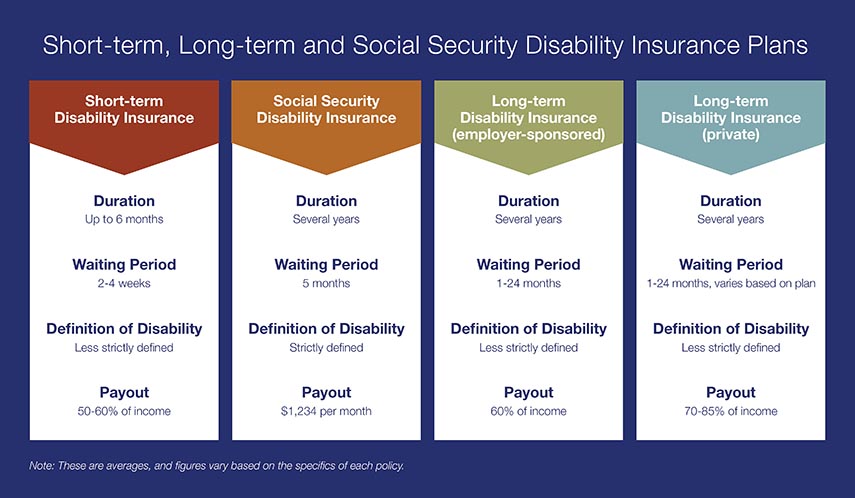

3. Long-term care insurance covers more healthcare costs than Medicare.

Medicare does not generally cover long-term care and will only pay for care at home under very limited circumstances.

Medicare does pay for skilled care in a nursing home only for short periods (up to 100 days) during which you are recuperating following a hospital stay for a related condition, but that’s not the same as long-term care. Once your care needs stabilize and you need personal or custodial care, Medicare will not pay those costs.

4. It’s likely you’ll need some form of long-term care.

A 65-year-old today has a 70% chance of needing long-term care services at some point during their lifetime.1 Because long-term care can be needed for many different reasons, it’s difficult to know if you’ll need it or not.

It’s better to purchase a LTCI policy when you’re still in good health — generally in your 50s — than to wait until you’re ill or older, when it may become unaffordable. The younger you are, the lower your premiums will be.

5. Your savings may not be enough to cover your long-term care needs.

There are various types of long-term care, from help with daily chores and activities to full care in a private nursing home room. The average assisted living facility costs $54,000 per year, and the average nursing home costs $94,900 per year for a semi-private room.4

With costs for long-term care on the rise, your retirement savings may not be big enough to cover these expenses.

6. The cost for long-term care insurance varies.

Pricing will depend on factors such as your age and the level of coverage the policy will pay out if you need to use it.

To give you an idea, the American Association for Long-term Care Insurance finds that a couple who opt for an initial policy benefit of $165,000, both age 55, will pay an annual premium of $2,080 combined. For a couple both age 65, the premium would rise to $3,750 per year.2

7. There are several type of long-term care insurance policies available.

A typical, traditional LTCI policy will pay a predetermined amount for each service — for instance, $100 a day for nursing home care. There generally will be a limit to the benefits you receive, either based on a number of years or a dollar amount. A plan that offers pooled benefits (meaning it covers more than one type of long-term care service) will set a total dollar amount for the various services you receive.

New types of LTCI policies are growing in popularity, extending beyond the traditional “use it or lose it” type, many of which have experienced premium increases.

One alternative is hybrid life and long-term care insurance. This type of policy combines long-term care insurance with permanent life insurance and provides more options:

- If you need long-term care, you can tap the policy benefit.

- If you die before needing long-term care, the policy has a life insurance benefit.

- If you decide you need the money for something else, you can typically receive a cash value that can be roughly equal to or less than the total premiums paid.

- Contract terms and premiums are guaranteed not to change.

Another alternative is a universal life insurance policy with a LTCI rider. This option might be right for you if you’re interested in a meaningful death benefit for your beneficiaries in the event LTCI isn’t needed.

At the end of the day, caregiving can take such an emotional and financial toll on loved ones that it pays to plan for long-term care now. Consider working with a financial professional to understand how traditional or alternative LTCI policies might fit into your current retirement strategy.

Learn more about your long-term care insurance options.