Retirement planning checklist

Review 18 important to-dos as you make your way toward retirement.

Why is insurance important in financial planning?

Just like your financial goals, insurance policies are as unique as you are.

Key takeaways

Women face unique challenges when it comes to retirement planning, including the “caregiver penalty,” a longer life expectancy and higher healthcare costs.

A financial advisor can help design a financial plan that is reasonable and achievable, taking some of the stress out of this major life event.

A comprehensive financial plan should include an emergency fund, regular tax-advantaged retirement savings and the proper insurance.

As you look ahead to retirement, it’s exciting to think about how you’ll spend your time, whether that’s with family and friends, enjoying hobbies or just relaxing during uninterrupted days. But as pleasant as that can be, there’s a lot of work you have to do to make those dreams into reality—and for many women, that can make planning for retirement feel more intimidating than exciting.

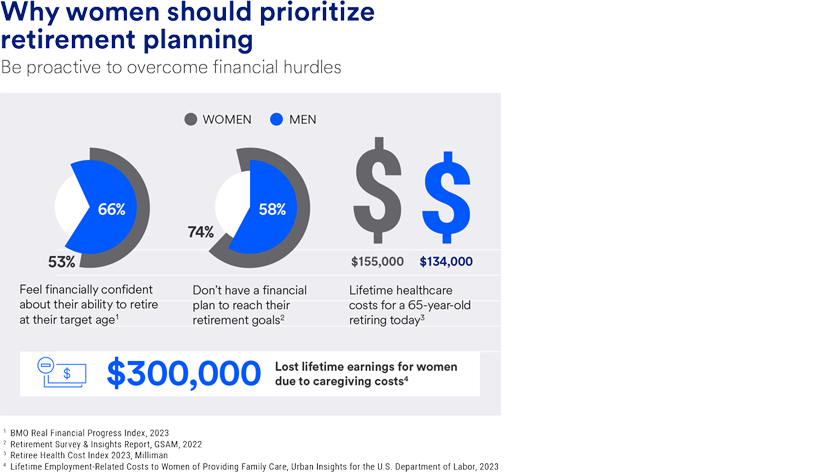

According to a special report by the BMO Real Financial Progress Index, only 53% of women feel financially confident about their ability to retire at their target age, compared with 66% of men.1 What’s more, 74% of women surveyed report having no financial plan in place to reach their retirement goals, compared with 58% of men.2

Women face unique challenges when it comes to planning for retirement, but these challenges don’t have to derail your plans.

There are numerous factors that can create obstacles for women planning for retirement. However, by recognizing these challenges and identifying meaningful steps to overcome them, women can confidently work toward a successful retirement.

Here’s what you should know about women preparing for retirement:

In the United States, women commonly take on the role of caregiver for children and elderly parents. Some 20% of all women workers in the U.S. are family caregivers, meaning women must balance both traditional employment and familial caregiving needs.3 In efforts to balance these demands, most caregivers must make numerous work-related adjustments, including using sick or vacation days, decreasing hours or missing workdays.4 In some cases, caregivers may even choose to leave the workforce entirely to provide care. These work adjustments can mean a significant economic impact on a woman’s finances. In fact, studies show that caregiving costs women nearly $300,000 in lost earnings over their lifetime.5

Women typically live about six years longer than men; U.S. women have a life expectancy of 79.3 years, while men have a life expectancy of 73.5 years.6 This difference means that women must often make their retirement savings last longer. And for those in a heterosexual relationship, they may face living and managing all costs alone on one income for some years.

According to the Retiree Health Cost Index, a 65-year-old woman retiring today should expect to spend about $155,000 on healthcare, versus the $134,000 that a 65-year-old man can expect..7 The biggest driver of this difference is not only the longer lifespan of women, but also the fact that women see their doctor more often during their lifetimes to seek out preventive care.

Growing healthcare costs also factor into this expense. According to National Health Expenditure Projections, national health spending is project to grow at an average of 5.5% per year over a 10-year period ending in 2027.8

Because many women are caregivers for children or family members, they experience at least $16,000 in lost wages annually because of the “motherhood wage gap.”9 At the same time, women are typically paid 83.7% of what men are paid.10 Because women are paid less on numerous fronts, they typically receive lower pension benefits.11

Unfortunately, women tend to be less prepared for the actual financial needs for their retirement. Lower lifetime earnings and decreased Social Security benefits are reflected in women’s retirement contributions, on average 30% less than men.12 Women also touch both ends of the spectrum of retirement savings: Half of women have no personal retirement savings, compared with 47% of men; and 22% of women have $100,000 in savings, versus 30% of men.13 Finally, women are also more likely to retire early and for reasons outside of their control, whether that be caregiving, job loss or health reasons.14

Taken together, these challenges can feel like an intimidating series of hurdles, but a successful retirement is possible for women with the right tactics.

Here are several retirement planning tips to keep in mind as you work toward a more secure retirement.

Retirement planning is about finding a balance between saving and then planning how to spend that money. Prepare for your retirement by considering the following pieces of your retirement:

Having a clear and attainable vision of what you want to achieve in retirement will help you stay focused on your goals.

Start investing early to take advantage of the power of compound growth. The good news is that women often hold their investments longer than men, helping them grow wealth over time.14

Consider these investing and savings options in your retirement plan:

Identify ways throughout your life that you can set aside money to create pockets of savings for the future. Keep in mind that diversification and asset allocation do not guarantee returns or protect against losses.

Even the best-laid retirement plans can be upended by unexpected expenses. Insurance serves as a potential safety net. Review your current insurance coverage to check for gaps, making sure to consider any dependents on your plan.

The list may include home, auto, umbrella, health, survivor income, disability, life, and long-term care insurance. Assess these policies every few years or following major life events to make sure you continue to have the coverage you need.

Retirement offers a much-deserved break from a lifetime of work, but the loss of a regular paycheck can be a difficult adjustment. Ensure you’re able to sustain your lifestyle by determining a reliable income stream and factoring it into your plan. Consider the following sources:

Use these sources to estimate the amount of income you could possibly generate and where you might encounter income gaps, helping you adjust your retirement plan accordingly.

It’s crucial as a woman planning for retirement to build a safety net in case of unexpected retirement road bumps. A general rule of thumb is to have three to six months of living expenses saved in an interest-earning savings account. This nest egg can provide security and an adequate cash fund during an emergency.

When planning for retirement, having a dedicated financial professional by your side can help you feel more prepared for your future.

According to Impact of Financial Professionals on Retirement Security, 40% of women who work with a financial professional report they feel very prepared for retirement, compared with 27% of women who don’t work with one.16While everyone’s retirement planning looks a little bit different, a strong relationship with your financial advisor can help you assess your personalized needs to formulate a plan that works best for you.

Women face unique challenges when it comes to planning for retirement, but these challenges don’t have to derail your plans. With careful planning and preparation, you can enjoy the retirement you’ve always dreamed of.

Learn how we can help put you on the path to the retirement you want.

Review 18 important to-dos as you make your way toward retirement.

Just like your financial goals, insurance policies are as unique as you are.