Key takeaways

A scholarship, inheritance or choosing a more affordable school are all reasons you might have unused 529 funds.

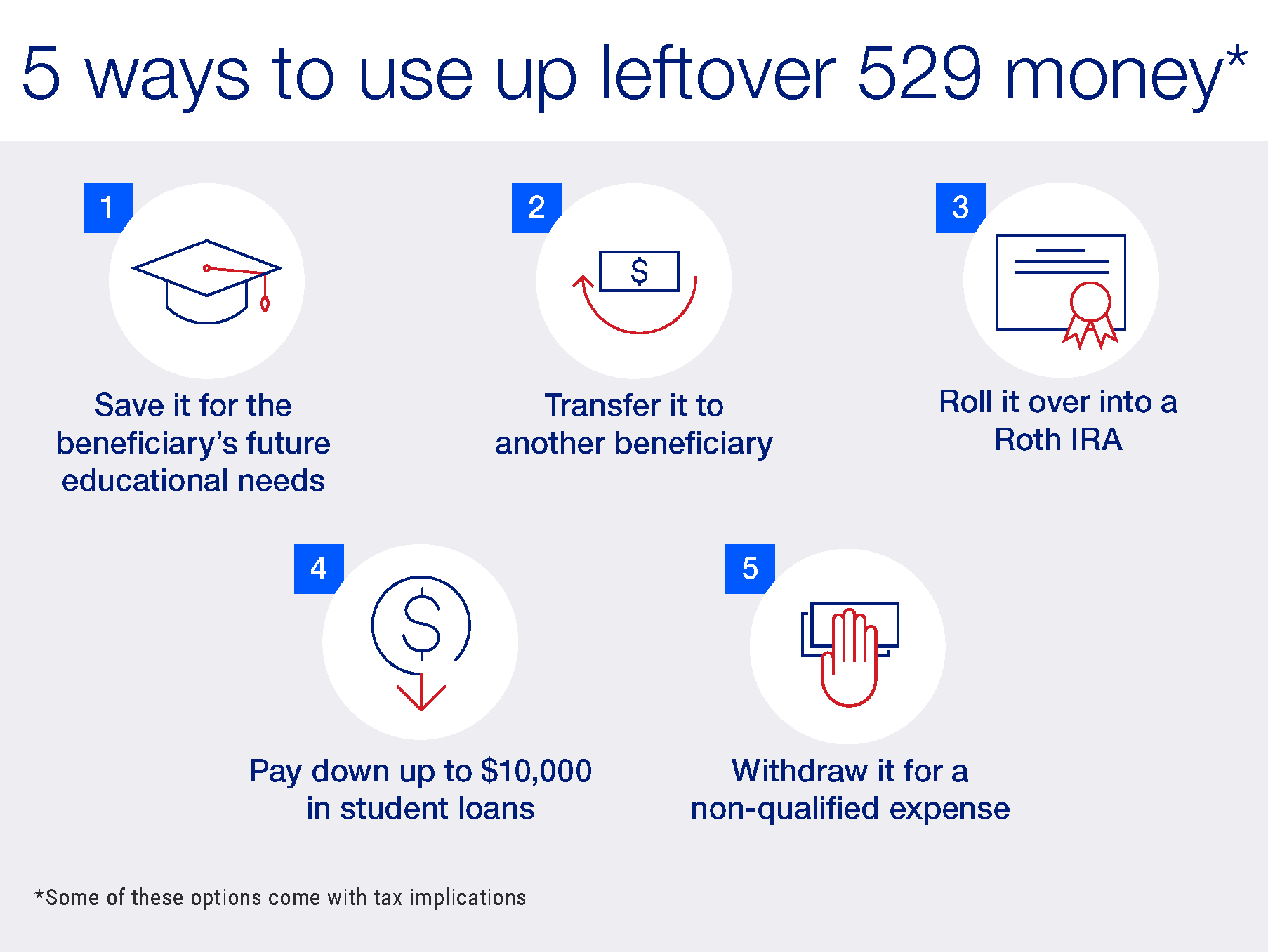

There are several ways to use up 529 funds, including transferring them to another beneficiary or rolling them over into a Roth IRA.

It’s best to consult a financial professional, as there could be tax impacts related to some of these options.

Tax-advantaged 529 education savings plans are a great way to start saving for your child’s higher education—especially considering the sharp rises in tuition over the years. But what happens to the 529 funds if they’re not used?

If your child received an unexpected scholarship, attended a more affordable in-state school or received an inheritance that went toward their education, you may wind up with leftover 529 plan funds in your account.

The good news is that you have options for your unused 529 funds, but there are some tax-related nuances to keep in mind.

“529 plans are quite flexible, because there's no time limit on when the funds have to be withdrawn from the account.”

Joni Meilahn, product management with U.S. Bancorp Investments

“There’s a myriad of reasons why there could be leftover funds in your 529 account, and fortunately there are also some good strategies for putting those funds to good use,” says Joni Meilahn, product manager with U.S. Bancorp Investments. “In fact, 529 plans are quite flexible, because there's no time limit on when the funds have to be withdrawn from the account.”

Don’t let leftover 529 money go to waste

One of the most obvious ways to use your unused 529 funds is to save them for future educational needs. If your child earned a bachelor’s degree, for example, they may want to enroll in a graduate school program and use the funds to cover some or all of that tuition.

You can also use 529 funds to pay for the beneficiary’s other educational expenses, including:

- Vocational training or trade school

- Certain room and board expenses

- Required textbooks

- Computers and software for educational purposes

- Up to $10,000 per beneficiary for elementary, middle or high school tuition

Of course, restrictions apply.

But if your child isn’t interested in adding more degrees to their resume, there are other ways to use up the funds left in a 529 account. Here’s how those different options work and the pros and cons of each.

Other options for using up leftover 529 funds

- Transfer the 529 account to a new beneficiary. If your child decides not to go to college or only uses part of the total funds while in school, you can transfer the remaining funds to another family member who is planning to attend college. “Just because the first beneficiary couldn’t use the 529 money, there's no reason why you can't switch the account over to a relative of the first beneficiary—or even change it to yourself as the beneficiary to use for classes on topics of interest to you, for example,” says Meilahn.

For example, the account owner can use the funds for any type of higher education, trade school or community college. “Those are all considered ‘qualifying education expenses’ for the purposes of a 529 plan,” she adds. While there’s no timeframe for when the money has to be withdrawn, you can only change the beneficiary twice a year, and the new one must be related to the original beneficiary. To ensure account continuity, you’ll also want to name a successor-owner. That way, the account will remain operational even if something were to happen to its initial owner.

- Make a 529 withdrawal for non-education expenses. If you’re in the middle of a home remodeling project or planning on a big purchase in the near future, the leftover funds in your 529 can be used to cover some or all of that expense. The money comes out prorated between contribution money and earnings, which means that only the “earnings” portion of the withdrawal is taxed.

“The earnings amount is added to ordinary income tax, and the earnings portion will generate a 10% penalty,” Meilahn says. “Granted, you don't want to have to pay a penalty at all and you do have to claim it as income for tax purposes, but that’s not that bad of a consequence if you absolutely need the money for non-qualified education expenses.”

The non-education withdrawal isn’t penalized if your child receives a scholarship (in other words, the money can be withdrawn to offset the scholarship amount), attends a U.S. military academy, becomes disabled or passes away.

- Use 529 funds to pay down any student loans. If you or a family member has an open student loan balance, you can use up to $10,000 of the leftover 529 funds to pay those loans down. Signed into law in 2022, the SECURE 2.0 Act allows funds to be used to pay off both federal and private student loans.

The new provision also allows account holders to pay off student loans borrowed by the beneficiary and their siblings, without having to change the name of the beneficiary. The leftover 529 funds can’t be used for other types of consumer loans (such as credit cards or personal loans).

- Roll the leftover 529 funds into a Roth IRA. Also new with the Secure 2.0 Act, you’ll be able to roll a portion of the unused 529 funds into a Roth IRA. There are some restrictions with this option, so be sure to check with your financial professional before making this move.

“There are some limitations on the Roth IRA contribution amount related to your 529, which has to have been in existence for at least 15 years prior to the rollover,” Meilahn points out. “This is a great use of the funds if there are some left over after a beneficiary is done with college.”

Regardless of how you plan to liquidate the funds remaining in your 529 account, an experienced financial professional can help you navigate the related complexities and make the right choice for your specific situation.

“If you try to DIY this, you may not be aware of the various guardrails, rules and regulations concerning 529s,” says Meilahn. “A financial professional will also explain the gifting tax consequences and help you better understand how the 529 plan operates within the context of your overall financial planning.”

Learn how our team-based planning approach can help you review financial opportunities from all perspectives.

For more information regarding college savings plans, please visit www.collegesavings.or. Participation in a 529 plan does not guarantee the investment return on contributions, if any, will be adequate to cover future tuition and other higher education expenses. Before investing in a 529 College Savings Plan, consider your state of residence, which may offer a 529 College Savings Plan with state tax or other benefits available only to residents of the state. Federal income tax on the earnings and a 10 percent penalty on distributions for non-qualified expenses may apply.

Tags:

Related articles

Roth IRA benefits: Roth IRA vs traditional IRA accounts

Unlike a traditional IRA, a Roth IRA allows you to contribute after-tax dollars now and withdraw contributions tax-free in retirement. Get details on Roth IRA contribution limits, Roth IRA income limits and Roth conversions.

Financial planning tips for the sandwich generation

Three tips on how to keep working toward your financial goals while supporting your children and aging parents.