A financial professional can help you develop a budget that’s sustainable and can carry you through retirement. DiGiorgio says she models out and compares a diverse range income and savings scenarios to show her clients what their future assets could look like under various conditions.

Often, she says, that information drives home just how important it is to think long-term about your spending. “We can show you ways to be secure in your future, while still having ‘play’ money that you can enjoy today,” she says.

Saving for future needs

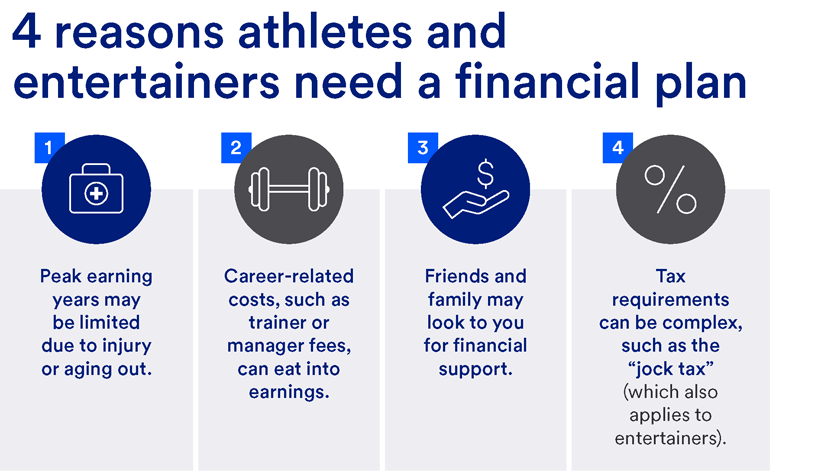

Even a top athlete may only play for 10 to 15 seasons. Entertainers typically have longer careers but have earnings that are less consistent.

The upshot: You may need to allocate a larger percentage of your income to retirement savings than most individuals. A financial professional can help you estimate what you’ll need to put away based on your projected retirement date and post-career expenses.

Some athletes have access to league-sponsored retirement accounts that can make it easier to set aside money for the future. However, entertainers usually don’t have those options, which requires them to pay even more attention to their long-term savings.

Because your situation can change significantly over time, consider meeting with your financial advisor regularly to make sure you’re saving adequately.

“You will want to revisit income, spending, retirement contributions and other forms of savings at least annually, to make sure you’re on track to achieve your long-term financial goals,” says DiGiorgio.

Paying the “jock tax”

The jock tax is an income tax that requires entertainers, athletes and other people associated with sports teams (such as trainers, coaches and doctors) to pay tax on money they earn outside their home states. For example, if you’re a resident in California but play a semifinal game in Illinois, Illinois would levy income tax on the money you earned during that game. All but five states levy this tax.

There’s no set jock tax percentage, so the amount you’ll have to pay depends on your base and bonus income, plus other factors such as how many games or performances you had in a particular state or city, and the tax rates in those states and cities.

This means that professional athletes and entertainers may have to file several state income tax returns for a single year.

Other complex tax requirements for athlete wealth management

Tax requirements can be much more complicated for athletes and entertainers than for others. Besides the jock tax, you may encounter tax-related issues including:

- Choosing where to live. When you receive base pay or a signing bonus, where you set up your main residence can have huge tax consequences. Some athletes and entertainers choose to establish their domicile in a state with no income tax to reduce what they owe.

- Preparing for estate taxes. You may leave behind millions of dollars in assets to your family. Depending on the value of your estate, there may be federal estate tax due that can be as high as 40% on a portion of your net worth. An estate planning professional can recommend strategies that make it easier for your loved ones to pay the tax, including life insurance trusts, without having to liquidate valuable assets. There are also ways to reduce the size of your estate while living to benefit your family in the future.

Creating a strategy to give back

As a successful athlete or entertainer, you develop a deep connection with your fan base. You may decide that you want to use some of your earnings to give back to the community that has supported you.

There are a lot of ways you can pursue your philanthropic endeavors, whether it’s contributing to a donor-advised fund, creating a charitable trust or establishing a private foundation. It’s important to talk with a professional you trust about the implications of your giving strategy. Your financial advisor can also help you screen charities to make sure your money is going to a reputable, tax-exempt organization.

Working with a financial advisor for athletes and entertainers

When you reach a certain level of success, your financial situation can feel overwhelming. Just as a successful company will hire a team of experts to manage their various needs — whether it’s investments, taxes, insurance or banking — you also need professionals who can guide you in these complicated areas.

You may be inclined to fill these financial roles with family members or friends as a way of showing your appreciation for their support. However, delegating that responsibility to people without the appropriate expertise often leads to self-dealing, personal bias in decision-making and improper reporting.

By hiring professionals with proper credentials, you’ll receive impartial financial advice you can trust. It’s worthwhile finding a financial planning team with experience in everything from financial planning and banking to trust services and philanthropy. They can help you put together a plan that encompasses everything from your peak earning years to a fulfilling and comfortable retirement.

“We want you to feel like you have a concierge for the financial side of your life,” says Wade.

Learn about working with a team of wealth specialists at U.S. Bank Wealth Management.