Effects of inflation on investments

Understanding yield vs. return

![]()

Interest rate fluctuations can send ripple effects throughout the economy. While the most recent interest rate hikes are meant to help curb inflation, it’s possible these effects could have an impact on stocks, bonds and other investments.

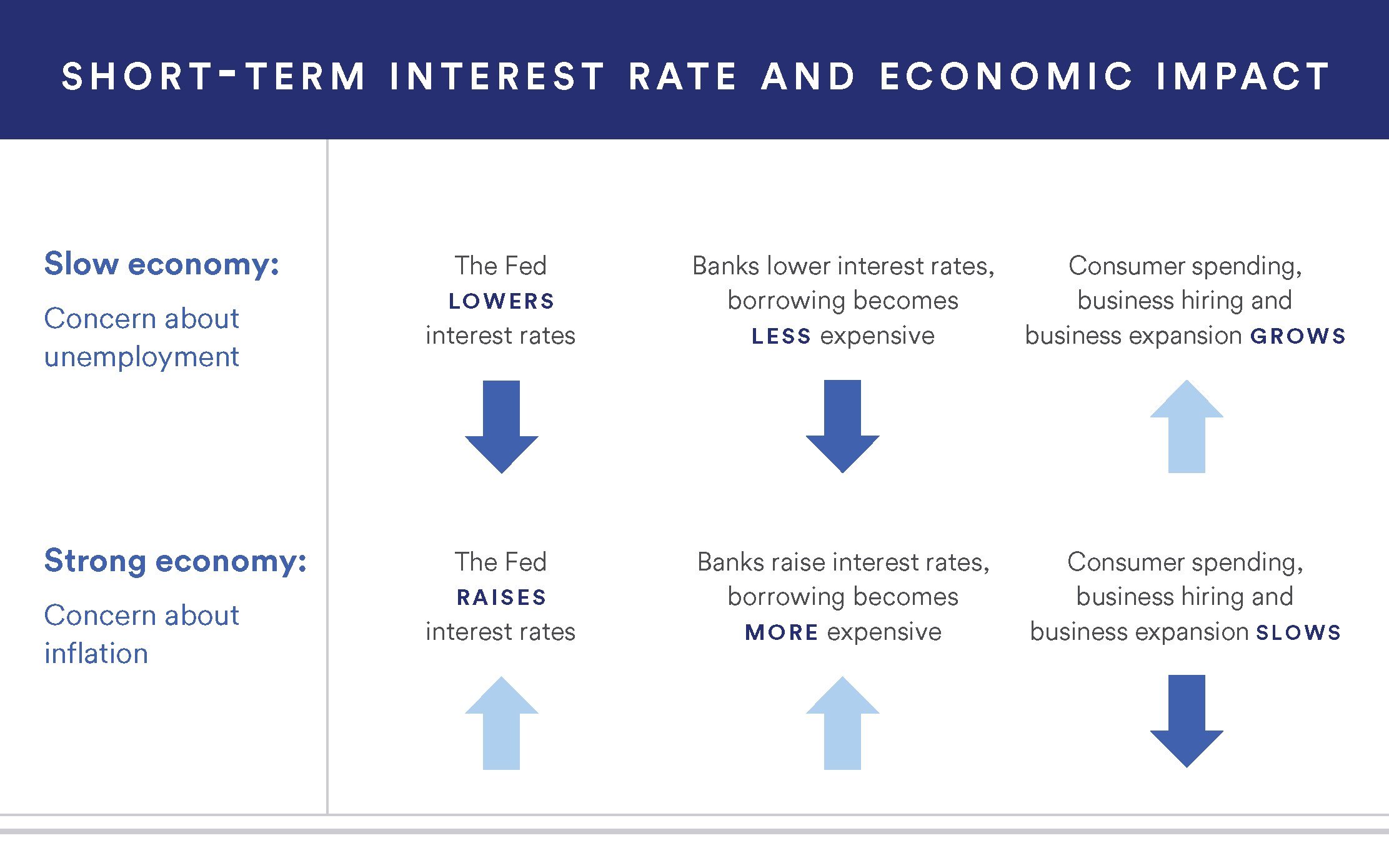

The Federal Reserve (the Fed) has a triple mandate: to promote maximum employment, stable prices and moderate long-term interest rates. One of the ways they do this is through adjusting short-term interest rates.

Reviewing the Fed’s previous actions shows how these scenarios map out. For example, leading up to and during the financial crisis in 2007 and 2008, the Fed drastically lowered rates to help jump-start a flagging economy. Eight years later, rates were still hovering close to zero. As the economy strengthened, the Fed raised interest rates nine times between 2015 and 2018.

More recently, the Fed cut interest rates three times in 2019 as the economy showed signs of slowing, and twice in 2020 – to near zero again – to curb the economic effects of the coronavirus pandemic.1 Current high inflation numbers have already led the Fed to increase interest rates for the first time since 2018, with additional hikes planned through 2023.

Given the recent ups and downs, it’s important to understand how interest rate changes can affect the components of your investment portfolio.

Interest rates and bonds have an inverse relationship: When interest rates rise, bond prices fall, and vice versa. Newly issued bonds will have higher coupons after rates rise, making bonds with low coupons issued in the lower-rate environment worth less.

It’s helpful to understand the following three concepts regarding the bond and interest rate relationship.

Read more about how rising interest rates impact the bond market..

In contrast to bonds, interest rate changes do not directly affect the stock market. However, Fed actions can have trickle-down effects that, in some cases, impact stock prices.

When the Fed raises interest rates, banks increase their rates for consumer and business loans. In theory, this means there’s less money available for consumer spending. Also, increased rates for business loans can sometimes cause companies to halt expansions and hires. Reduced consumer and business spending can both lower the value of a company’s stock.2

Still, there’s no guarantee that a rate hike will negatively impact stocks. Typically, rising interest rates occur during periods of economic strength. In this scenario, increased rates often coincide with a bull market. With a balance of stocks and bonds, your portfolio may be better positioned to maintain more stability despite an interest rate increase.

Read more about the current effect of rising interest rates on the stock market.

In addition to stocks and bonds, consider how rate changes might affect other elements in your portfolio.

|

Interest rates raised |

Interest rates lowered |

|---|---|

|

|

Interest rates raised

Interest rates lowered

Because interest rate fluctuations can affect investments in different ways, there is no single action you should take when they change.

Stay focused on your financial goals, stick to your plan, and work with your financial professional to construct a portfolio that is diversified enough to help weather any short-term effects of a rate change.

Your investment strategy should reflect your goals, risk tolerance and time horizon. Learn how our approach to investment management can help you achieve your vision of success.

Related content